Industria Construcción en Colombia

26

Colomb ia - Construction 0078 - 2801 - 2015 ! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 1 MarketLine Industry Profile Construction in Colombia January 2016 Reference Cod e: 0078-2801 Publication Date: January 2016 WWW.MARKETLINE.COM MARKETLINE. THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCO PIED A Progressiv e Digital Media business

Transcript of Industria Construcción en Colombia

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 1/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 1

MarketLine Industry Profile

Construction in

ColombiaJanuary 2016

Reference Cod e: 0078-2801

Publication Date: January 2016

WWW.MARKETLINE.COM MARKETLINE. THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED

A Progressive Digital Media business

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 2/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 2

!"!#$%&'! )$**+,-

*./012 3.451The Colombian construction industry grew by 6.4% in 2015 to reach a value of $28.3 billion.

*./012 3.451 67/18.92In 2020, the Colombian construction industry is forecast to have a value of $38.7 billio n, an increase of 36.7% since

2015.

#.21:7/; 91:<1=2.2>7=Civil engineering is the largest segment of the construction industry in Colombia, accounting for 45.5% of the industry's

total value.

?17:/.@A; 91:<1=2.2>7=Colombia accounts for 1.8% of the Americas construction industry value.

*./012 />3.4/;The construction industry is fragmented.

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 3/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 3

TABLE OF CONTENTS

Executive Summary..........................................................................................................................................................................2

Market value ..................................................................................................................................................................................2

Market value forecast...................................................................................................................................................................2

Category segmentation................................................................................................................................................................2

Geography segmentation ............................................................................................................................................................2

Market ri valry .................................................................................................................................................................................2

Market Overview ...............................................................................................................................................................................7

Market definition............................................................................................................................................................................7

Market analysis .............................................................................................................................................................................7

Market Data........................................................................................................................................................................................8

Market value ..................................................................................................................................................................................8

Market Segm entation .......................................................................................................................................................................9

Category segmentation................................................................................................................................................................9

Geography segmentation ..........................................................................................................................................................10

Market Outlook ................................................................................................................................................................................11

Market value forecast.................................................................................................................................................................11

Five Forces Analysis ......................................................................................................................................................................12

Summary ......................................................................................................................................................................................12

Buyer power.................................................................................................................................................................................13

Supplier power ............................................................................................................................................................................14

New entrants ...............................................................................................................................................................................15

Threat of substi tutes...................................................................................................................................................................16

Degree of rivalry ..........................................................................................................................................................................17

Leading Companies........................................................................................................................................................................18

Constructora Conconreto ..........................................................................................................................................................18

Grupo Odinsa ..............................................................................................................................................................................19

Techint Engineering & Construction ........................................................................................................................................20

Macroeconomic Indicators.............................................................................................................................................................21

Country Data ...............................................................................................................................................................................21

Methodology ....................................................................................................................................................................................23

Industry associations..................................................................................................................................................................24

Appendix...........................................................................................................................................................................................25

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 4/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 4

About MarketLine........................................................................................................................................................................25

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 5/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 5

LIST OF TABLES

Table 1: Colombia construction industry value: $ billion, 2011 –15...........................................................................................8

Table 2: Colombia construction industry category segmentation: $ billion, 2015...................................................................9

Table 3: Colombia construction industry geography segmentation: $ billion, 2015 .............................................................10

Table 4: Colombia construction industry value forecast: $ billion, 2015 –20 .........................................................................11

Table 5: Constructora Conconreto: key facts .............................................................................................................................18

Table 6: Grupo Odinsa : key facts ................................................................................................................................................19

Table 7: Techint Engineering & Construction: key facts ...........................................................................................................20

Table 8: Colombia size of population (million), 2011 –15..........................................................................................................21

Table 9: Colombia gdp (constant 2005 prices, $ billion), 2011 –15.........................................................................................21

Table 10: Colombia gdp (current prices, $ billion), 2011 –15 ...................................................................................................21

Table 11: Colombia inflation, 2011 –15 ........................................................................................................................................22

Table 12: Colombia consumer price index (absolute), 2011 –15.............................................................................................22

Table 13: Colombia exchange rate, 2011 –15 ............................................................................................................................22

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 6/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 6

LIST OF FIGURES

Figure 1: Colombia construction industry value: $ billion, 2011 –15 .........................................................................................8

Figure 2: Colombia construction industry category segmentation: % share, by value, 2015 ...............................................9

Figure 3: Colombia construction industry geography segmentation: % share, by value, 2015 .........................................10

Figure 4: Colombia construction industry value forecast: $ billion, 2015 –20 ........................................................................11

Figure 5: Forces driving competition in the construction industry in Colombia, 2015..........................................................12

Figure 6: Drivers of buyer power in the construction industry in Colombia, 2015 ................................................................13

Figure 7: Drivers of supplier power in the construction industry in Colombia, 2015 ............................................................14

Figure 8: Factors influencing the likelihood of new entrants in the construction industry in Co lombia, 2015 ..................15

Figure 9: Factors influencing the threat of substitutes in the construction industry in Colombia, 2015 ............................16

Figure 10: Drivers of degree of rivalry in the cons truction industry in Colombia, 2015 .......................................................17

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 7/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 7

*+,B!% C'!,'&!D

*./012 E16>=>2>7=The construction industry is defined as the value of work put in place annually in the residential, non -residential, and civil

engineering segments. The residential segment covers houses, dwellings, and similar work. The non -residential segment

covers commercial, industrial, social, and similar work. Civil engineering covers infrastructure for transportation,

telecommunications, energy, and other purposes.

New build and also renovation and repair are included. The industry includes construction of buildings and engineering

structures themselves, and also preparatory work and completion (demolition, site preparation, electrical and plumbing

installation, etc). However, property development and construction materials are not part of this industry.

All currency conversions were carried out at constant average annual 2014 exchange rates.

For the purposes of this report, North America consists of Canada, Mexico, and the United States.

South America comprises Argentina, Brazil, Chile, Colombia, and Venezuela.

Europe comprises Austria, Belgium, the Czech Republic, Denmark, Finland, France, Germany, Greece, Ireland, Italy,

Netherlands, Norway, Poland, Portugal, Russia, Spain, Sweden, Switzerland, Turkey, and the United Kingdom.

Scandinavia comprises Denmark, Finland, Norway, and Sweden.

Asia-Pacific comprises Australia, China, Hong Kong, India, Indonesia, Kazakhstan, Japan, Malaysia, New Zealand,

Pakistan, Philippines, Singapore, South Korea, Taiwan, Thailand, and Vietnam.

Middle East comprises Egypt, Israel, Saudi Arabia, and United Arab Emirates.

The global market consists of North America, South America, Europe, Asia -Pacific, Middle East, South Africa and

Nigeria

*./012 .=.4;9>9Colombia has posted healthy growth in its construction industry in recent years, a trend set to continue through to 2020.

The Colombian construction industry had total value of $28.3bn in 2015, representing a compound annual growth rate

(CAGR) of 4% between 2011 and 2015. In comparison, the US and Mexican industries grew with CAGRs of 6.5% a nd

1% respectively, over the same period, to reach respective values of $1,024.1bn and $40.0bn in 2015.

In 2012, the government announced a two-year plan to construct free residential units for 100,000 of the country's

poorest people. This will have boos ted industry values in those years.

The civil engineering segment was the industry's most lucrative in 2015, with total value of $12.9bn, equivalent to 45.5%

of the industry's overall value. The residential segment contributed value of $7 .9bn in 2015, equating to 27.9% of the

industry's aggregate value.

The performance of the industry is forecast to accelerate, with an anticipated CAGR of 4.4% for the five-year period 2015

- 2020, which is expected to drive the industry to a value of $16.0bn by the end of 202 0. Comparatively, the US and

Mexican industries will grow with CAGRs of 5.2% and 2.9% respectively, over the same period, to reach respectivevalues of $1,318.3bn and $46.1bn in 2020.

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 8/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 8

*+,B!% F+%+

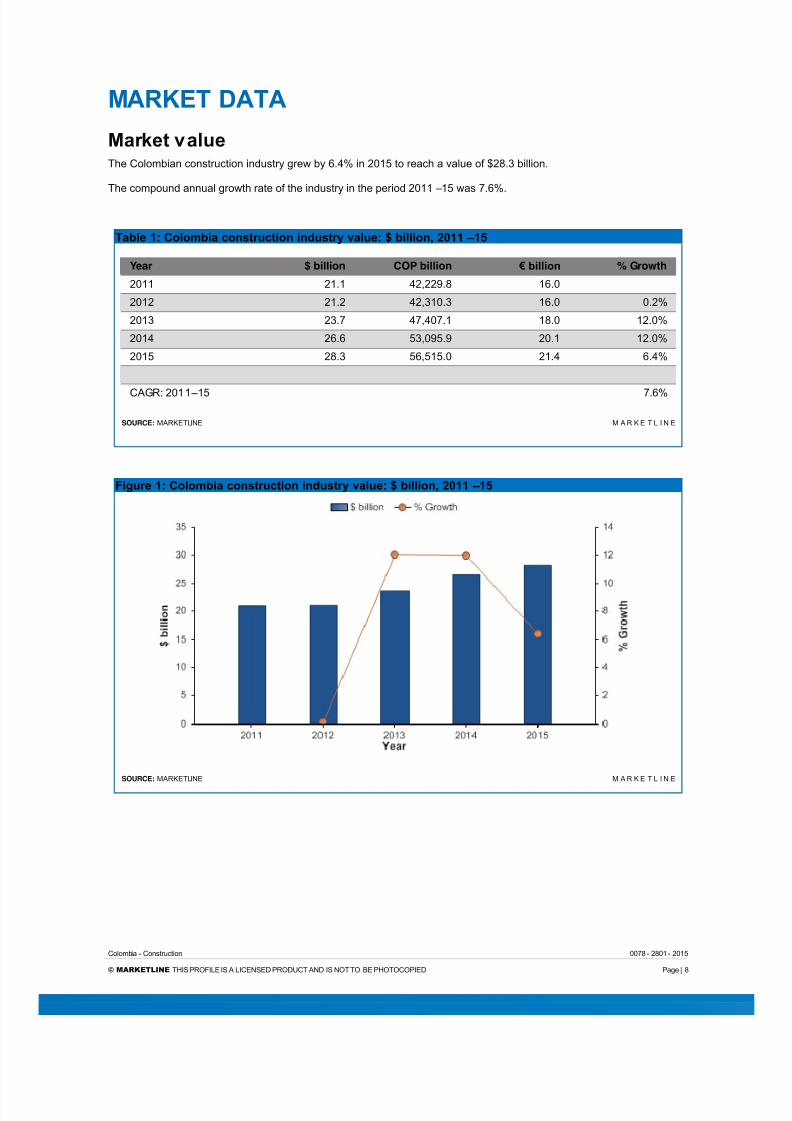

*./012 3.451The Colombian construction industry grew by 6.4% in 2015 to reach a value of $28.3 billion.

The compound annual growth rate of the industry in the period 2011 –15 was 7.6%.

%.G41 HI #747<G>. 87=92/582>7= >=E592/; 3.451I J G>44>7=K LMHH –HN

Year $ billion COP billion € billion % Growth

2011 21.1 42,229.8 16.0

2012 21.2 42,310.3 16.0 0.2%

2013 23.7 47,407.1 18.0 12.0%

2014 26.6 53,095.9 20.1 12.0%

2015 28.3 56,515.0 21.4 6.4%

CAGR: 2011 –15 7.6%

SOURCE: MARKETLINE M A R K E T L I N E

O>:5/1 HI #747<G>. 87=92/582>7= >=E592/; 3.451I J G>44>7=K LMHH –HN

SOURCE: MARKETLINE M A R K E T L I N E

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 9/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 9

*+,B!% )!?*!P%+%&CP

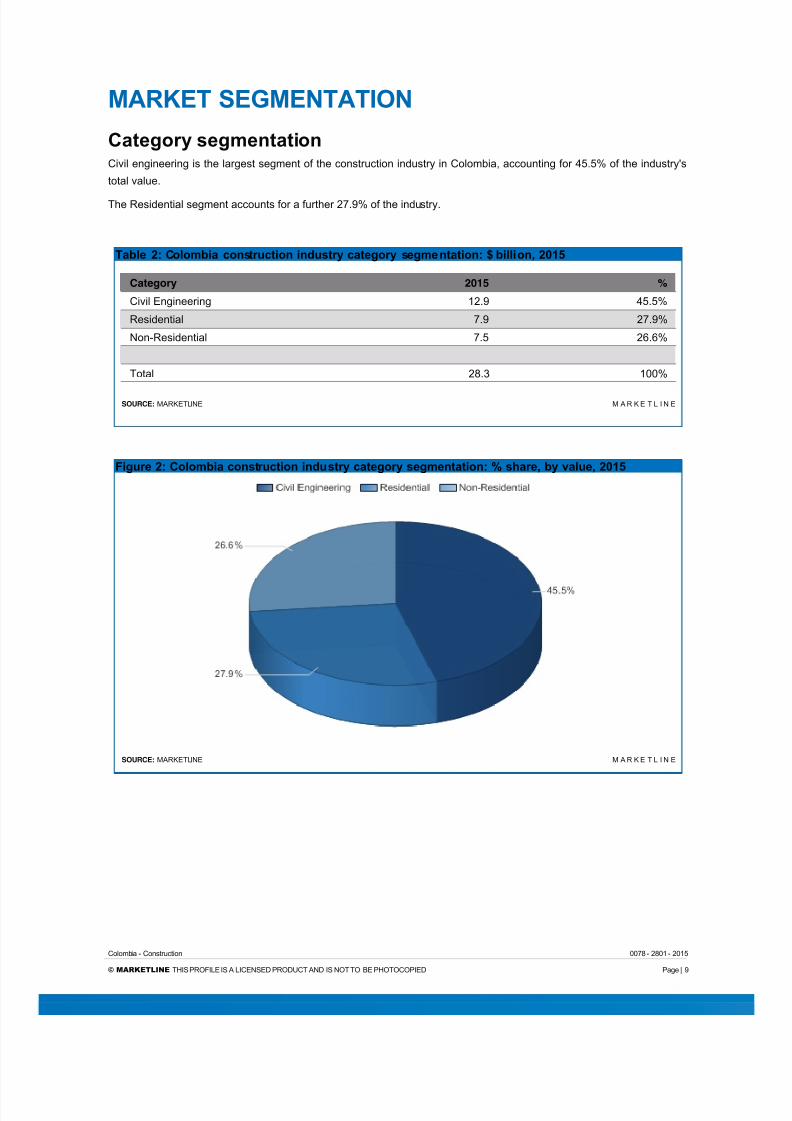

#.21:7/; 91:<1=2.2>7=Civil engineering is the largest segment of the construction industry in Colombia, accounting for 45.5% of the industry's

total value.

The Residential segment accounts for a further 27.9% of the industry.

%.G41 LI #747<G>. 87=92/582>7= >=E592/; 8.21:7/; 91:<1=2.2>7=I J G>44>7=K LMHN

Category 2015 %

Civil Engineering 12.9 45.5%

Residential 7.9 27.9%

Non-Residential 7.5 26.6%

Total 28.3 100%

SOURCE: MARKETLINE M A R K E T L I N E

O>:5/1 LI #747<G>. 87=92/582>7= >=E592/; 8.21:7/; 91:<1=2.2>7=I Q 9A./1K G; 3.451K LMHN

SOURCE: MARKETLINE M A R K E T L I N E

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 10/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 10

?17:/.@A; 91:<1=2.2>7=Colombia accounts for 1.8% of the Americas construction industry value.

The United States accounts for a further 63.6% of the Americas industry.

%.G41 RI #747<G>. 87=92/582>7= >=E592/; :17:/.@A; 91:<1=2.2>7=I J G>44>7=K LMHN

Geography 2015 %

United States 1,024.1 63.6

Brazil 153.3 9.5

Mexico 40.0 2.5

Colombia 28.3 1.8

Rest of the Americas 365.4 22.7

Total 1,611.1 100.1%

SOURCE: MARKETLINE M A R K E T L I N E

O>:5/1 RI #747<G>. 87=92/582>7= >=E592/; :17:/.@A; 91:<1=2.2>7=I Q 9A./1K G; 3.451K LMHN

SOURCE: MARKETLINE M A R K E T L I N E

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 11/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 11

*+,B!% C$%SCCB

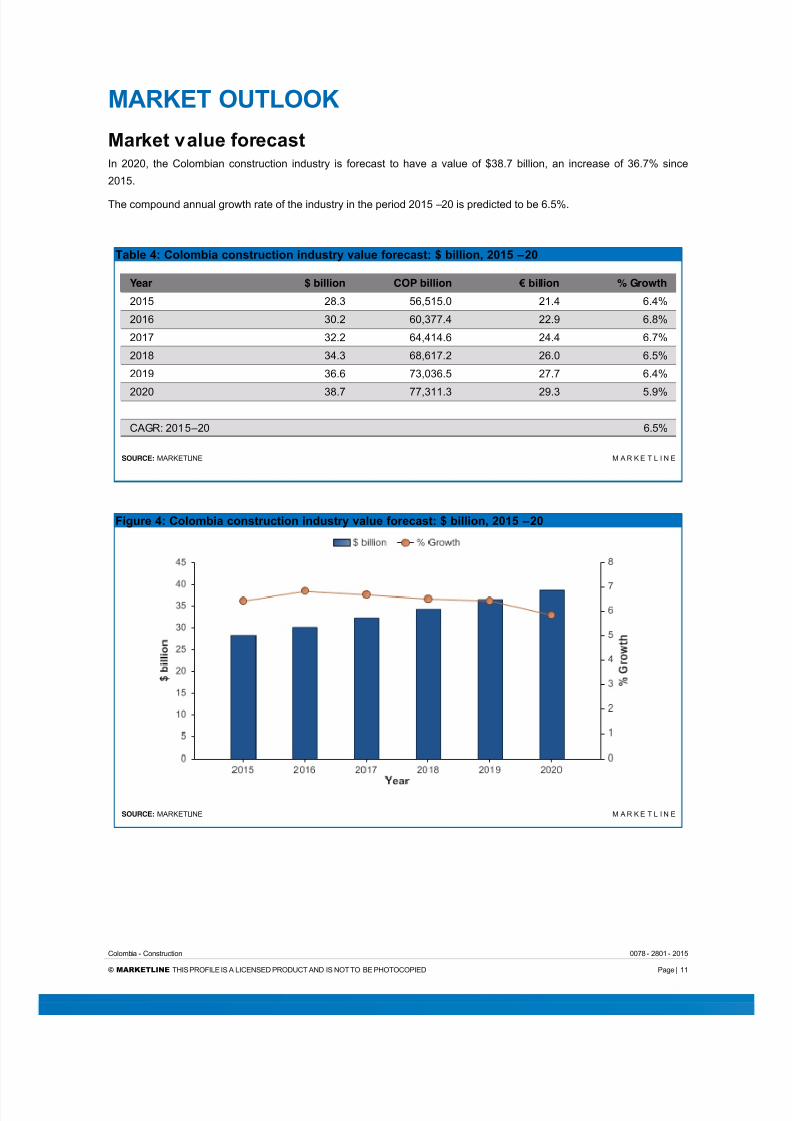

*./012 3.451 67/18.92In 2020, the Colombian construction industry is forecast to have a value of $38.7 billion, an increase of 36.7% since

2015.

The compound annual growth rate of the industry in the period 2015 –20 is predicted to be 6.5%.

%.G41 TI #747<G>. 87=92/582>7= >=E592/; 3.451 67/18.92I J G>44>7=K LMHN –LM

Year $ billion COP billion € billion % Growth

2015 28.3 56,515.0 21.4 6.4%

2016 30.2 60,377.4 22.9 6.8%

2017 32.2 64,414.6 24.4 6.7%

2018 34.3 68,617.2 26.0 6.5%

2019 36.6 73,036.5 27.7 6.4%

2020 38.7 77,311.3 29.3 5.9%

CAGR: 2015 –20 6.5%

SOURCE: MARKETLINE M A R K E T L I N E

O>:5/1 TI #747<G>. 87=92/582>7= >=E592/; 3.451 67/18.92I J G>44>7=K LMHN –LM

SOURCE: MARKETLINE M A R K E T L I N E

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 12/26

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 13/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 13

U5;1/ @7V1/

O>:5/1 WI F/>31/9 76 G5;1/ @7V1/ >= 2A1 87=92/582>7= >=E592/; >= #747<G>.K LMHN

SOURCE: MARKETLINE M A R K E T L I N E

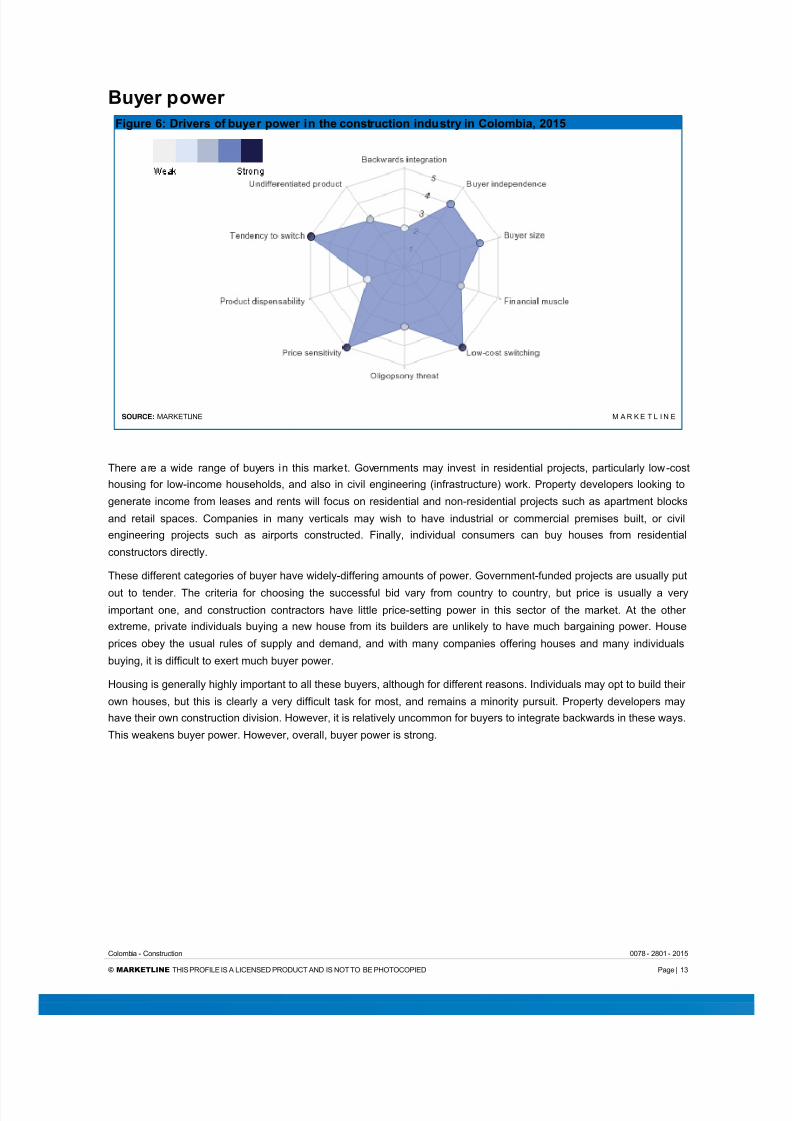

There are a wide range of buyers in this market. Governments may invest in residential projects, particularly low-cost

housing for low-income households, and also in civil engineering (infrastructure) work. Property developers looking to

generate income from leases and rents will focus on residential and non-residential projects such as apartment blocks

and retail spaces. Companies in many verticals may wish to have industrial or commercial premises built, or civil

engineering projects such as airports constructed. Finally, individual consumers can buy houses from residential

constructors directly.

These different categories of buyer have widely-differing amounts of power. Government-funded projects are usually put

out to tender. The criteria for choosing the successful bid vary from country to country, but price is usually a very

important one, and construction contractors have little price-setting power in this sector of the market. At the other

extreme, private individuals buying a new house from its builders are unlikely to have much bargaining power. House

prices obey the usual rules of supply and demand, and with many companies offering houses and many individuals

buying, it is difficult to exert much buyer power.

Housing is generally highly important to all these buyers, although for different reasons. Individuals may opt to build their

own houses, but this is clearly a very difficult task for most, and remains a minority pursuit. Property developers may

have their own construction division. However, it is relatively uncommon for buyers to integrate backwards in these ways.

This weakens buyer power. However, overall, buyer power is strong.

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 14/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 14

)5@@4>1/ @7V1/

O>:5/1 XI F/>31/9 76 95@@4>1/ @7V1/ >= 2A1 87=92/582>7= >=E592/; >= #747<G>.K LMHN

SOURCE: MARKETLINE M A R K E T L I N E

For prime contractors, suppliers include producers of building materials and also sub -contractors who offer specialist

construction competencies.

The cons truction materials sector is typical ly concentrated. Cement and similar materials are commoditized. Their

production benefits from s cale economies, and there are additional gains if a supplier has a well -developed dis tribution

system, notably a network of ready-mix concrete facilities. In these circumstances, consolidation is favored and it is

common to find just four or five companies dominating cement production in a country. In Colombia, ten companies

account for all domestic cement capacity, although Cementos Argos Colombia owns much or all of the equity in eight of

these. This increases their supplier power.

In contrast, construction companies of all types tend to be small and numerous, for reasons discussed in the New

Entrants section. This means that prime contractors will generally have a wide choice of competing sub-contractors for

any part of the project. Supplier power is weakened in this situation.

Supplier power is also weakened by the fact the construction industry is very important to supplier revenues, there are

few other markets where they can generate their revenues.

On the other hand, there are few substitutes available. If the price of cement rises, a construction company cannot switch

to brick and build the project as designed. There are no alternatives to the services offered by sub -contractors. Overall,

supplier power is moderate.

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 15/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 15

P1V 1=2/.=29

O>:5/1 YI O.827/9 >=6451=8>=: 2A1 4>014>A77E 76 =1V 1=2/.=29 >= 2A1 87=92/582>7= >=E592/; >=#747<G>.K LMHN

SOURCE: MARKETLINE M A R K E T L I N E

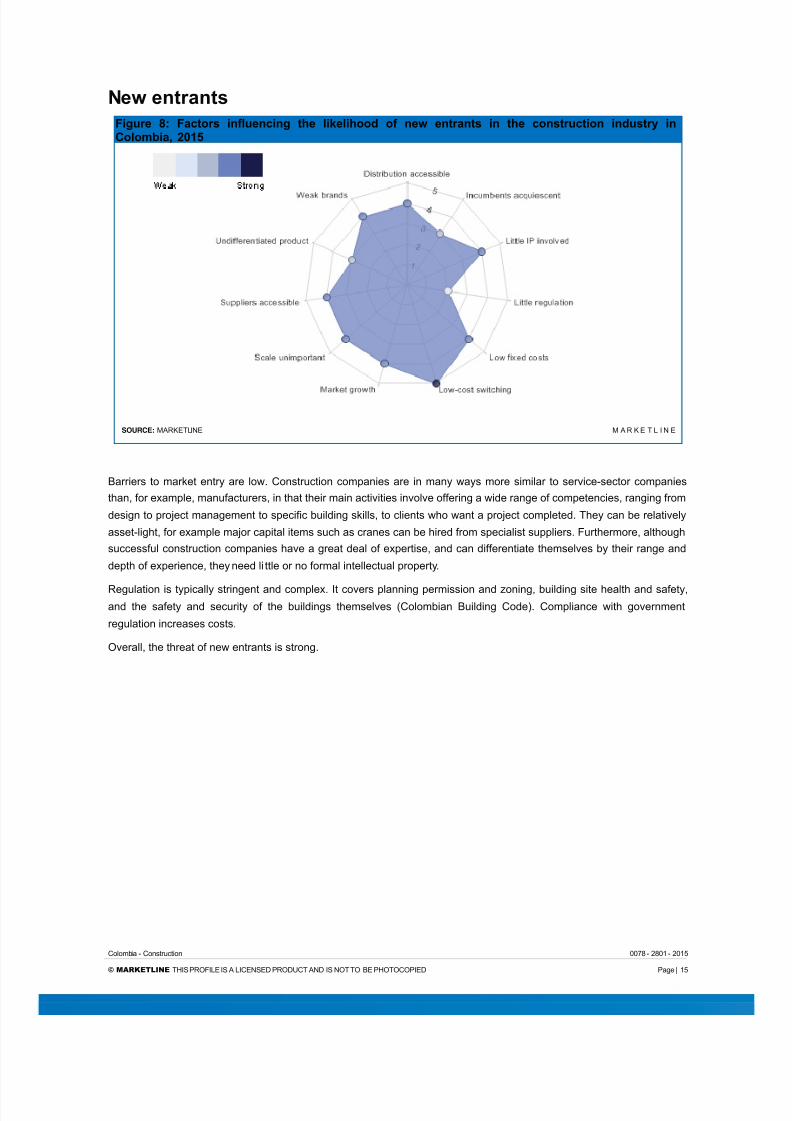

Barriers to market entry are low. Construction companies are in many ways more similar to service-sector companies

than, for example, manufacturers, in that their main activities involve offering a wide range of competencies, ranging from

design to project management to specific building skills, to clients who want a project completed. They can be relatively

asset-light, for example major capital items such as cranes can be hired from specialist suppliers. Furthermore, although

successful construction companies have a great deal of expertise, and can differentiate themselves by their range and

depth of experience, they need li ttle or no formal intellectual property.

Regulation is typically stringent and complex. It covers planning permission and zoning, building site health and safety,

and the safety and security of the buildings themselves (Colombian Building Code). Compliance with government

regulation increases costs.

Overall, the threat of new entrants is strong.

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 16/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 16

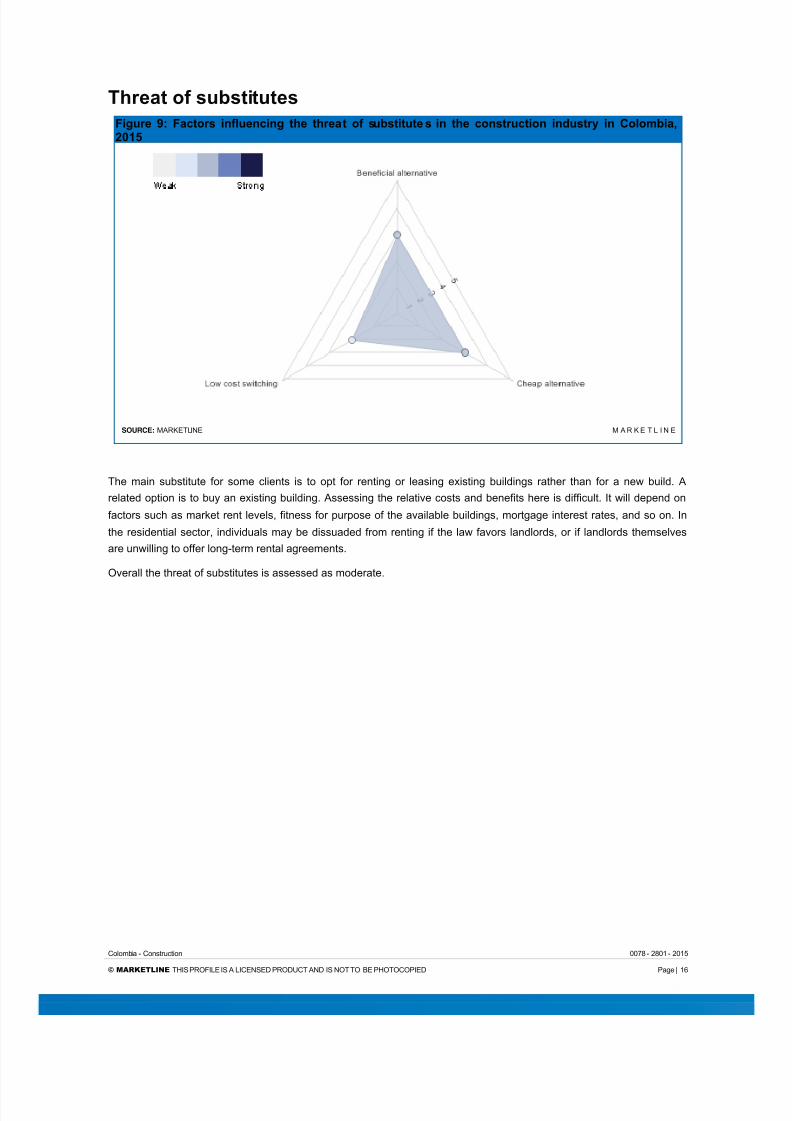

%A/1.2 76 95G92>25219

O>:5/1 ZI O.827/9 >=6451=8>=: 2A1 2A/1.2 76 95G92>2521 9 >= 2A1 87=92/582>7= >=E592/; >= #747<G>.KLMHN

SOURCE: MARKETLINE M A R K E T L I N E

The main substitute for some clients is to opt for renting or leasing existing buildings rather than for a new build. A

related option is to buy an existing building. Assessing the relative costs and benefits here is difficult. It will depend on

factors such as market rent levels, fitness for purpose of the available buildings, mortgage interest rates, and so on. In

the residential sector, individuals may be dissuaded from renting if the law favors landlords, or if landlords themselves

are unwilling to offer long-term rental agreements.

Overall the threat of substitutes is assessed as moderate.

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 17/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 17

F1:/11 76 />3.4/;

O>:5/1 HMI F/>31/9 76 E1:/11 76 />3.4/; >= 2A1 87=92/582>7= >=E592/; >= #747<G>.K LMHN

SOURCE: MARKETLINE M A R K E T L I N E

With a large number of small companies alongside the large players, all offering similar services, rivalry is expected to be

strengthened in the construction market.

Many companies have diversified in terms of the market segments they operate in, as similar competencies are required

in building projects with different end-uses. However, all segments tend to be affected in an economic downturn (there

may be an exception if a government responds to recession by increasing its spending on particular types of

construction). Geographic diversification can offer more protection against the vagaries of any one country market, but

may be difficult for the typically small construction firm. These factors mean that when macroeconomic conditions are

tough, rivalry will tend to increase significantly.

Furthermore, i t is fairly easy for market players to ramp their output up and down in response to demand. Employees

may be taken on for individual projects, for example, rather than being retained permanently on the payroll. Overall, the

degree of rivalry is assessed as moderate.

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 18/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 18

S!+F&P? #C*[+P&!)

#7=92/5827/. #7=87=/127%.G41 NI #7=92/5827/. #7=87=/127I 01; 6.829

Head office: Carrera 43A No. 18Sur-135, Piso 4 Sao Paulo Plaza, Medellín, COLTelephone: 57 574 402 5700

Website: www.conconcreto.com

Financial year-end: December

Ticker: CONCONC:CB

Stock exchange: Bolsa Colombia

SOURCE: COMPANY WEBSITE M A R K E T L I N E

Constructora Conconreto is a construction company headquartered in Medellin, Colombia. It is also active in Panama. In

FY2014, the company had a workforce of 1,998 employees.

Its construction activities are divided into infrastructure and buildings. Its infrastructure projects include highways,

tunnels, and bridges, hydropower generation plants, and airports. Building projects include residential, commercial,

institutional, and industrial works.

The company also has a property development business, which builds, operates, and rents out commercial, retail, and

hospitality spaces.

Its Concreto Ambiental division offers mobile and compact water treatment systems.

Key Metrics

In FY2014, the company posted revenues of COP785,739m ($393m), an increase of 27.4% on the previous year. Net

income was COP51,809 ($26m), a decrease of 14.5% on FY2013. Further financials are unavailable.

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 19/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 19

?/5@7 CE>=9.

%.G41 WI ?/5@7 CE>=9. I 01; 6.829

Head office: Carrera 14 No. 93A -30, Bogotá D.C., COL

Telephone: 571 650 1919

Website: www.odinsa.com

SOURCE: COMPANY WEBSITE M A R K E T L I N E

Grupo Odinsa is a civil engineering company headquartered in Bogota, Colombia.

The company holds several concessions to design, build, maintain, and operate highways. These include 270 km of

roads in the coffee-growing regions of Colombia, the 123 km Boulevard Turistico del Atlantico in the Dominican Republic,

and roadway, bridge, and tunnels in La Pintada, Colombia.

Its Port Corporation of Santa Marta division operates, maintains and extends the marine port of Santa Marta in

Magdalena, Colombia. Odinsa has a similar role for Eldorado International Airport in Colombia and Tocumen Airport in

Panama.

In the energy sector, the company operates GENA and GENPAC, thermal power stations located in Panama and Chile,

respectively.

Odinsa Projects and Investments is responsible for the Instituto Nacional de Vías (INVIAS), the National Institute of

Roadways, which collects tolls from users of certain roads in Colombia.

Key Metrics

In FY2014, the company posted revenues of COP919,906m ($460m), an increase of 5.3% on the previous year. Net

income rose by 11.5% to COP102,200m ($51m).

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 20/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 20

%18A>=2 !=:>=11/>=: \ #7=92/582>7=

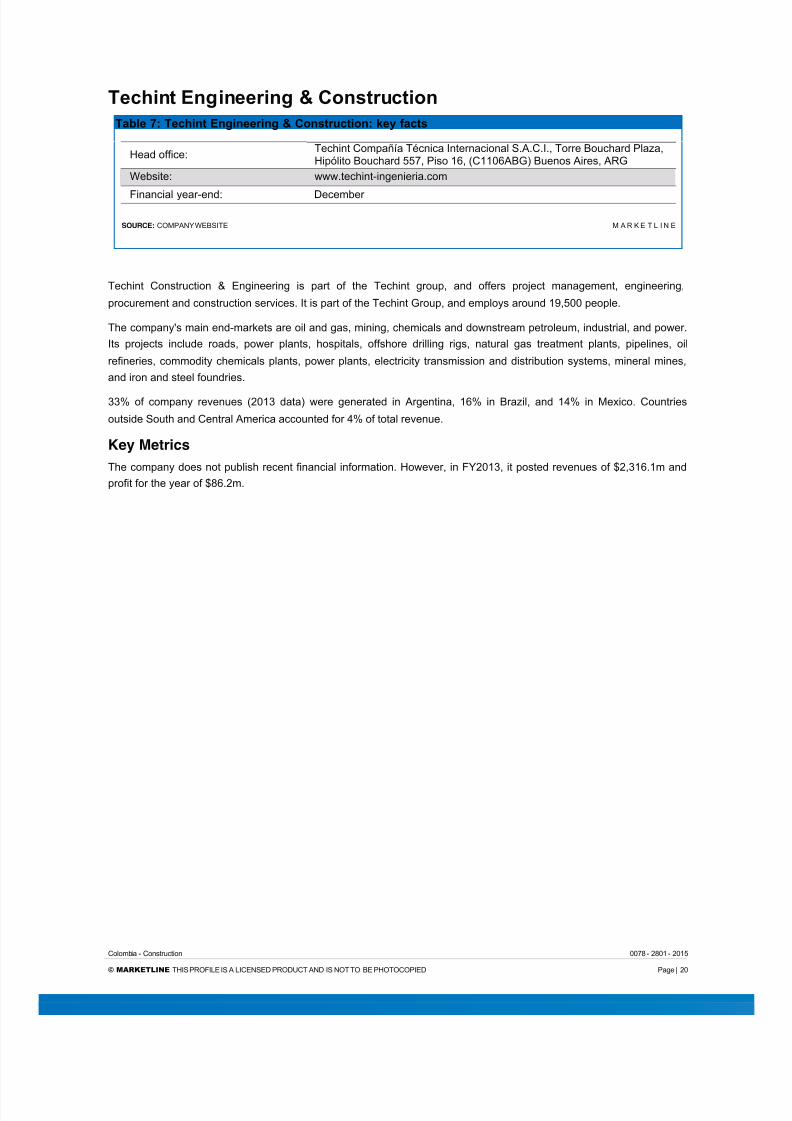

%.G41 XI %18A>=2 !=:>=11/>=: \ #7=92/582>7=I 01; 6.829

Head office:Techint Compañía Técnica Internacional S.A.C.I., Torre Bouchard Plaza,Hipólito Bouchard 557, Piso 16, (C1106ABG) Buenos Aires, ARG

Website: www.techint-ingenieria.com

Financial year-end: December

SOURCE: COMPANY WEBSITE M A R K E T L I N E

Techint Construction & Engineering is part of the Techint group, and offers project management, engineering,

procurement and construction services. It is part of the Techint Group, and employs around 19,500 people.

The company's main end-markets are oil and gas, mining, chemicals and downstream petroleum, industrial, and power.

Its projects include roads, power plants, hospitals, offshore drilling rigs, natural gas treatment plants, pipelines, oil

refineries, commodity chemicals plants, power plants, electricity transmission and distribution systems, mineral mines,

and iron and steel foundries.

33% of company revenues (2013 data) were generated in Argentina, 16% in Brazil, and 14% in Mexico. Countries

outside South and Central America accounted for 4% of total revenue.

Key Metrics

The company does not publish recent financial information. However, in FY2013, it posted revenues of $2,316.1m and

profit for the year of $86.2m.

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 21/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 21

*+#,C!#CPC*&# &PF&#+%C,)

#75=2/; F.2.

%.G41 YI #747<G>. 9>]1 76 @[email protected]>7= ^<>44>7=_K LMHH –

HN

Year Population (million) % Growth

2011 46.0 1.2%

2012 46.6 1.2%

2013 47.1 1.2%

2014 47.7 1.1%

2015 48.2 1.1%

SOURCE: MARKETLINE M A R K E T L I N E

%.G41 ZI #747<G>. :E@ ^87=92.=2 LMMN @/>819K J G>44>7=_K LMHH –HN

Year Constant 2005 Prices, $ billion % Growth

2011 195.0 6.6%

2012 202.9 4.0%

2013 212.9 4.9%

2014 222.6 4.6%

2015 228.5 2.7%

SOURCE: MARKETLINE M A R K E T L I N E

%.G41 HMI #747<G>. :E@ ^85//1=2 @/>819K J G>44>7=_K LMHH –HN

Year Current Prices, $ billion % Growth

2011 335.4 16.9%

2012 369.4 10.1%

2013 380.0 2.9%2014 377.9 (0.6%)

2015 391.9 3.7%

SOURCE: MARKETLINE M A R K E T L I N E

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 22/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 22

%.G41 HHI #747<G>. >=64.2>7=K LMHH –HN

Year Inflation Rate (%)

2011 3.4%

2012 3.2%

2013 2.0%

2014 2.9%

2015 4.6%

SOURCE: MARKETLINE M A R K E T L I N E

%.G41 HLI #747<G>. 87=95<1/ @/>81 >=E1` ^.G974521_K LMHH –HN

Year Consumer Price Index (2005 = 100)

2011 129.8

2012 133.9

2013 136.6

2014 140.6

2015 147.1

SOURCE: MARKETLINE M A R K E T L I N E

%.G41 HRI #747<G>. 1`8A.=:1 /.21K LMHH –HN

Year Exchange rate ($/COP) Exchange rate (€/COP)

2011 1,827.4900 2,542.4000

2012 1,798.2500 2,312.1800

2013 1,869.4100 2,483.8400

2014 1,997.8300 2,637.0800

2015 1,997.8300 2,637.0800

SOURCE: MARKETLINE M A R K E T L I N E

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 23/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 23

*!%aCFCSC?-

MarketLine Industry Profiles draw on extensive primary and secondary research, all aggregated, analyzed, cross -

checked and presented in a consistent and accessible style.

Review of in-house databases – Created using 250,000+ industry interviews and consumer surveys and supported by

analysis from industry experts using highly complex modeling & forecasting tools, MarketLine’s in -house databasesprovide the foundation for all related industry profiles

Preparatory research – We also maintain extensive in-house databases of news, analyst commentary, company

profiles and macroeconomic & demographic information, which enable our researchers to build an accurate market

overview

Definitions – Market defin itions are standardized to allow comparison from country to country. The parameters of each

definition are carefully reviewed at the start of the research process to ensure they match the requirements of both the

market and our clients

Extensive secondary research activities ensure we are always fully up-to-date with the latest industry events and

trends

MarketLine aggregates and analyzes a number of secondary information sources, including:

- National/Governmental statistics

- International data (official international sources)

- National and International trade associations

- Broker and analyst reports

- Company Annual Reports

- Business information libraries and databases

Modeling & forecasting tools – MarketLine has developed powerful tools that allow quantitative and qualitative data to

be combined with related macroeconomic and demographic drivers to create market models and forecasts, which can

then be refined according to specific competitive, regulatory and demand-related factors

Continuous quality control ensures that our processes and profiles remain focused, accurate and up-to-date

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 24/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 24

&=E592/; .9978>.2>7=9

Camara Colombiana de la Construccion

Carrera 19 # 90 - 10 Piso 2-3, Edificio Camacol, Bogotá D.C., COL

Tel.: 57 1 743 0265

Fax: 57 1 217 2813

camacol.co

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 25/26

Colombia - Construction 0078 - 2801 - 2015

! #$%&'()*+' THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 25

+[[!PF&"

+G752 *./012S>=1In an information-rich world, finding facts you can rely upon isn’t always easy. MarketLine is the solution.

We make it our job to sort through the data and deliver accurate, up-to-date information on companies, industries and

countries across the world. No other business information company comes close to matching our sheer breadth of

coverage.

And unlike many of our competitors, we cut the ‘data padding’ and present information in easy-to-digest formats, so you

can absorb key facts in minutes, not hours.

What we do

Profiling all major companies, industries and geographies, MarketLine is one of the most prolific publishers of business

information today.

Our dedicated research professionals aggregate, analyze, and cross -check facts in line with our strict research

methodology, ensuring a constant stream of new and accurate information is added to MarketLine every day.

With stringent checks and controls to capture and validate the accuracy of our data, you can be confident in MarketLineto deliver quality data in an instant.

For further information about our products and services see more at: http://www.marketline.com/overview/

Disclaimer

All Rights Reserved.

No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form by any means,

electronic, mechanical, photocopying, recording or otherwise, without the prior permission of the publisher, MarketLine.

The facts of this report are believed to be correct at the time of publication but cannot be guaran teed. Please note that

the findings, conclusions and recommendations that MarketLine delivers will be based on information gathered in good

faith from both primary and secondary sources, whose accuracy we are not always in a position to guarantee. As such

MarketLine can accept no liability whatever for actions taken based on any information that may subsequently prove to

be incorrect.

8/16/2019 Industria Construcción en Colombia

http://slidepdf.com/reader/full/industria-construccion-en-colombia 26/26

MarketLine | John Carpenter House, John Carpenter Street |London, United Kingdom, EC4Y 0ANT: +44(0)203 377 3042, F: +44 (0) 870 134 4371