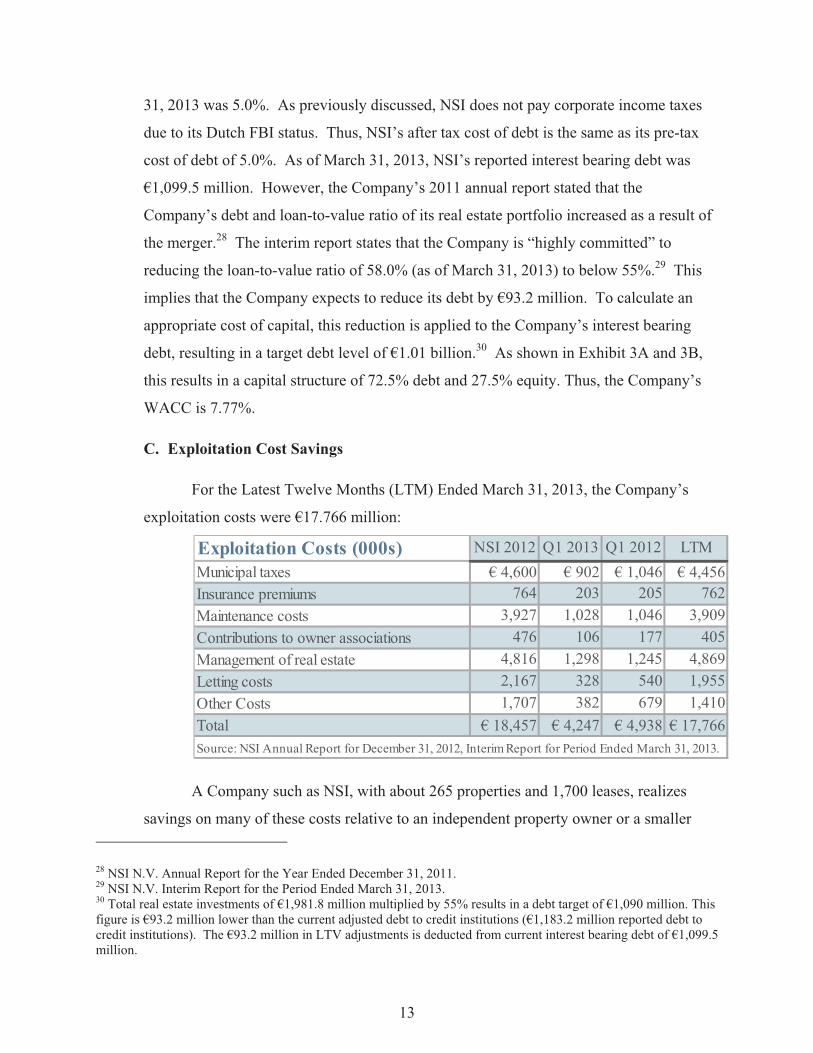

Legge... · ˇ ˇˇ˚ˇ ˘ ˇ #˝˝ ˘ ˇ ˘ #ˇ ˇ ˘ ˝ ˇ # ˚ ˚ˇ ˘ ˇ ˜ ˙ˇ # ˇ ˇ˙ ˜4 ˚ ˇˇ

2013������31���������� ��������1960����� ����

����������

����� ������������������� ��� ���� �

��������� ��� ��� ���� �

��������������������������� ��� �� � �

�������������������������� ��� �� � �

� ��� ���������������������� ��� �� � ��

����� �������� ���� ���������

����� ������������������� ������� �

������ �)1960 ( �"�

("���")

���� ��� ���� ��������

� ������� ����� ��/� ���� � ����� ���� ���� ����� � ��� ���"� " ����� ���� ����� � ������� ��

�� �����2012 ") ���������� (" ����� �� ����� ���������� �� �� ����� ���� ��1:

1.����� 1.9 ���� ������ ���� �����- ����� ������ ������ ������ ������

����8.5.2013 ����� ����� �� � ���� ����� � ���� ������ ����� ���� ����� ����� ,

���� ��� ����� ������12.5.2013 � ������ ���� � � �� � ���� ���� ������ ,����� ,�����

���� ������� ������ �������� ����� ���� ����������� ��������18.3.2013 ���� ���

������� ������� �� ����� ���� ����� ������ ������ �� ��� �� ������ ���� �� � �����

���� .�� ����9.5.2013 � ����� ���� �� ����� ���� �� � ���� ����� ���� ����19.5.2013

��� � � ������ ������ ���� �� � ����� ���� :���� � �� ����� ���� � ����� �� � ���

�� �) ��� ����� ������ ���� ��� ���� ����� ��� � ��� ����� (��� �� ��) ���� �����12 � (

��� , ��� ������ ������� ���� ����� � �� ��� ���� � ���� �� ���� ����� ) �� �12(

���� �) ��� �� ���� �� ������26.7.2013.(

��� ��� ���� ��� ,����� ������ ����� ����� �8.5.2013 :������ '��)2013-01-057256� ( -

9.5.2013 :������ '��)2013-01-058957����� �� �� ������ ��� ������ �� ,(.

����13.5.2013 ������� ����� ���� �� �� �� �) ���� ������12����� � ( ���� �� �

������ ��� ����� ��� � ���� ���� ����� ) �� �12( ���� ������ ����� ��� �� ��� ,

31.5.2013, ����17.6.2013 . ������ '��) � ���� ���� � ��� ����� ������2013-01-061825 �� (

����� �� �� ������ �� ������.

����17.5.2013 ���� � ���� ����� ������ ������ ����� ����� ���� ���� ����� ����� �

���� ����� �������19.5.2013 .���� ��� ����� �������� � ��� ���� ����� ����� ��

17.5.2013 ������ '��)2013-01-063592( �����19.5.2013 ������ '��)2013-01-063898 �� (

����� �� �� ������ �� ������.

����19.5.2013 ���� ������ ����� ���� ����� ����� � ���� �� �� � �� �� ����� �

��� ����� � ���� ����� ������ � ������ ������ ����� � � �� ������ ����� �� ����

������ '��) � ���� ���� � ��� ����� ������ .��� �� �� ��� ������2013-01-064339 �� (

.����� �� �� ������ �� ������

1 ��� � ��� ����� ���� ���� �����39� ���� �������� ���� ) ��� ����� ����� ���"�� ,(�-1970. ���� ��� �� ���

�� � ��� ������ ������ ���� �� �� � ������ ��������� ������ ��� ,���� ����� ���� � ��� ����� �� ����� �� ����� � �������2012 ���� ����� ��28 ,����2012 :������)2013-01-021751.(

- 2 -

2.����� 1.9 ���� ������ ���� �����- ����� ������ ������ ������ ������������ 15.3.3 -

(� �����) ���� �� �����

����21 ,������2013 �� ��������� ��� ����� ������ �� �)4,��� ����� ( ����� ����� ����

�� �) ���� ������4 (- ������ �.�.� �� �� ����2007 �"�� �� ,� ���� '��3 ������ �� ���� ,

�� �) ���� ����� ������� ���� ��/� ����� ���� �� �� ��4 � ��� �� ������� �� ���� (

,�"��� ������������ ���� ��� ���� ������� �� �� ������ ������ �� �� �� ������� ��

��� ��� ������ ���� ���� ,�������� � ���� ��������.������ ����� �� � ���� �� �����

����� ��� ��� ���� ��� ,����� ������10.4.2013 :������ '��)2013-01-032932 ;(14.4.2013

:������ '��)2013-01-035992 ;(17.4.2013 ) '�� ������2013-01-035992� (- 21.4.2013 ) '��

������: 2013-01-040159 �- 2013-01-041107.(

- 3 -

3.� ����.27.6 ������ ���� ����� ����- ��� ������� ����� - �� ������� ������City Plaza

:����� ����� �������

��� ������ �������100% �� .��� ������- 74%

����31.3.2013 ����31.12.2012 ����31.12.2011 ����31.12.2010

��� ������� �����) ��� ����(������

51,960 54,94054,69054,400

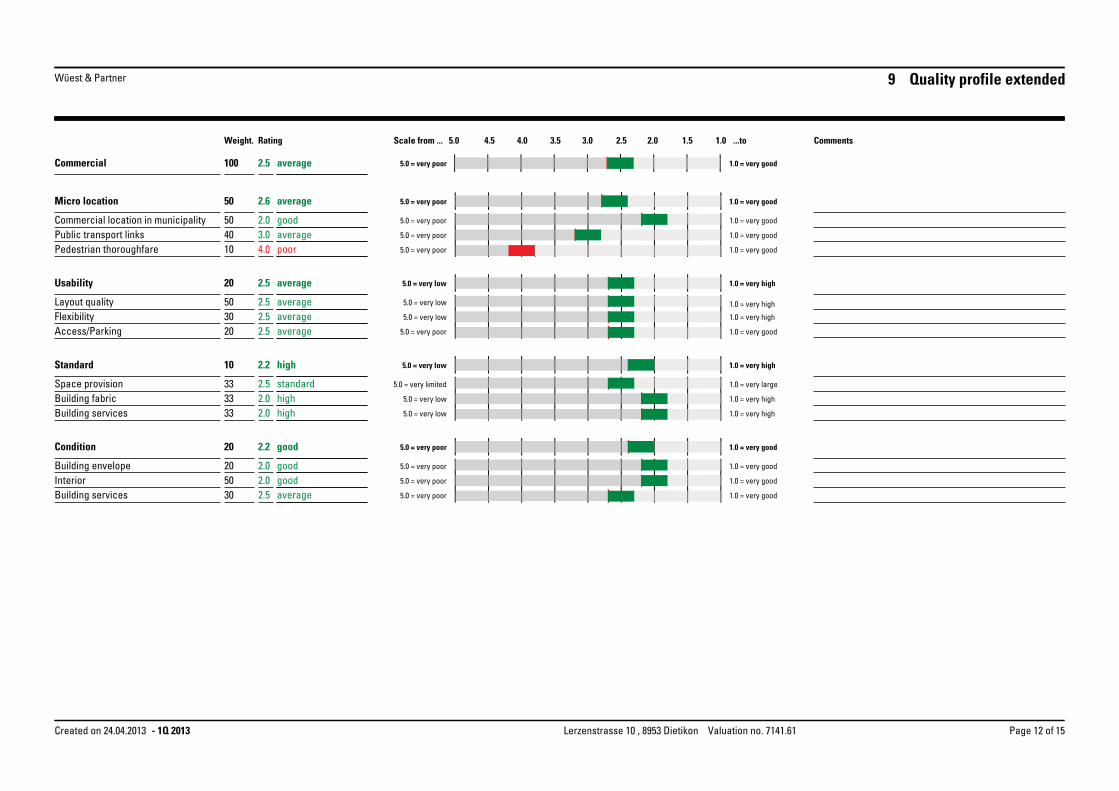

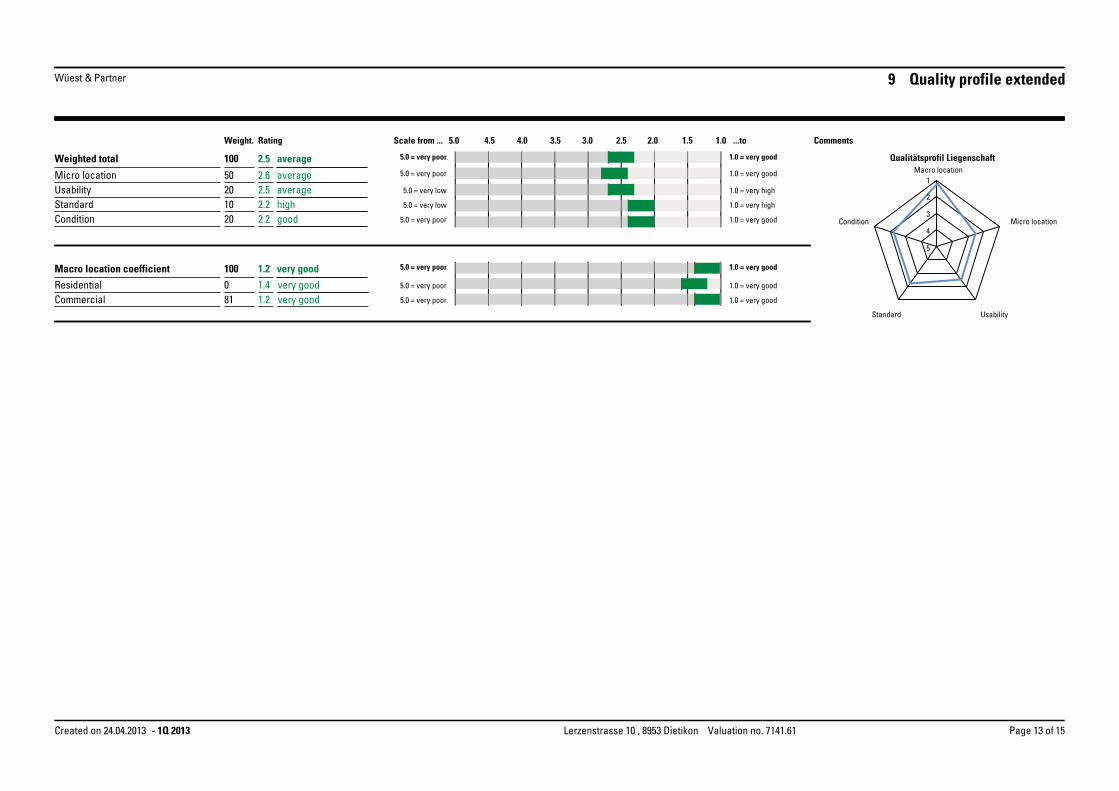

���� ����� ����Wuest & Partner

Wuest & Partner

Wuest & PartnerWuest & Partner

?���� ���� ������ ����� �� �� �� ?���� ���� ���� �����������

���� ����� � ����� ����� ����� ������� ���� ������)

(����

31/3/201331/12/201231/12/201131/12/2010

���� ����� � ��DCF DCF DCF DCF ����� ����� ����� ����� ������� �������

���� ������ ���� ������-

Sales Comparison Approach

�� ��- ����

)Gross Leasable Area ��� (

����� �����(�"�)

12,74412,74412,74412,744

����� ����� ���� �� ��� ����-

����� ���� ��� �����

95%95%98% 98.2%

(����) ����� �� ������� ������� ����� ����� �"�� ���) ��� �����

(������

203203198 199

����� ����4.7% 4.4%4.6%4.8% NOI ����� �����

����) ��� �����(������ ���

2,415 2,4022,579 2,579

�� ���� ������ �����- NOI

��� � �����)NOI ���� ����

(��� ���

4.65% 4.37%4.7%4.8%

������� ������1% 1%1%1% ����� ����) ����� ������ �����

:(���� ���� ����� ���� ���� �����������

����� ����� � ����5%*55,558 57,69055,70054,400 � � ���5%49,362 52,20051,95051,680

����� ����� � ����5%55,558 57,69057,42057,120 � � ���5%49,362 52,20051,95051,680

����� �� �������

����

� ����5%55,558 57,69057,42057,120 � � ���5% 49,362 52,20051,95051,680

� ����� ����� *5% � ����� � ��- 100% .������ ���� ,�����

- 4 -

4. �����10.1.7 ������ ���� ����� ����- �����- .NSI N.V ")NSI("- ������

����26 ������2013 � ���� ����� ���� ����� ����NSI ���� � ��� �� ����� ��� �

�NSI���� , ����� ��� ��� )LTV � (NSI � ����- 55%, ��� � ����� ������ ��� � ����

85% �- 100% ��� ��� .������ ���� ������ ,������ ���������- LTV ����� ����- 55% � ���� -

60% � ����� ��� ����� ,50% �������� ������ ������. ��� ����- LTV �� ����60%

����� ��� ����� �50% ����� ������ �������� .

���� � ��� �� ��� ,����� ������29.4.2013 :������ '��)2013-01-047218 �� ������ �� ,(

.����� �� �� ������

5.������� 31.1.01 �- 15.6 ���� ������ ���� �����- ��� ����� ����- NSI ������� �

����� ,�������

) �� ����� ���� ���� �����Refinance (� ��� �� ���19 ,��������2012 ���Habas Tulip

B.V ��� �� � �� ��� � ���� � ���� ���� , � ����� ����� � � �� (�������) ��������

74% ")Habas Tulip("� ���� �� �� ���� ��������� �� ,- Habas Tulip ������ �����

�����NSI �������Habas Tulip ) ������ � ��� ����LtSV ������� ���� ��� ���� �� ���� ,(

���� � ������� ����� ���� ( ����� �� ���� ���� �����)NSI � ���� �� ,50%.

���� ����� ����������� � ���- 50% � � �� ����� ,Habas Tulip ����5 ,������2013� � �� , -

700 � � �� ��� �� ���� ���� ����� � ����) ���� ���� - 518 ������ ���� ����� (���� ����

� � �� �� ��� ����� �� ���� �� �� ����� ���� .������ � ��� ���� � ���� - 18,914,720

� ,����� ��� - LtSV � ���� ��49.93%.

����1.5.2013�������� ��� �� ,������ ���� �������� ���� ����� ����� , �� ��� �����

����� ����� ���� � �� ������ ��� �� ���� ������� ����� ����� ��� '� � �

NSI���� ������� ������ ���� ��� �� ,.

� �������� ��� ,������ � ����� �� ����� ��� �7.4.2013 :������ '��)2013-01-027499( � -

1.5.2013 :������ '��)2013-01-050569(� ������ �� ,�� .����� �� �� ������

6. �����10.2.2.2 ������ ���� ����� ����- ������ ����� ��� ������

����10 ������2013 �����- Habas Star B.V � ����� ����� � � �� ������� ����74%

")Habas Star(", ���� ������ ����� ��������)30%( �- HORN Three Management GmbH �-

HORN Three GmbH & Co. KG ����� ,��� ���� ��� �� ,����� �� � �� ��� � ����

� � ��� ������ ����- 1.27 � ��������� ,��� �� �� ��� ������ �����, �� � �� �- 0.27

��� ���� ���� �� ����� ���� ������ ��� ���� ����) ����� �������� (���� ��. �����

� ���� ���� ���� �� ����� - Habas Star ���� ������� � ����� ,�� ,����� ��� ����� ;

� � ��� ��� ������ ���� - 0.27 .���� ������

- 5 -

���� � ��� �� ��� ,����� ������11.4.2013 :������ '��)2013-01-033286 �� ������ �� ,(

.����� �� �� ������

7. �����13.2)1( ������ ���� ����� ����- ������ �����

���� 1 ����2013 ����Habas Star � ��� ���� ������1 ���� ������ ���� ���� ��� � ���� ��

") �"�� �"� (��) ���� � � �� �� "��� ����(" ���� �� �� ��� ������� ���� �� ��11 ,�������

2013 ")������� ����,���� .(" ���� �� �� �� ����� ������ ��� �������� ������� 31 ,����

2013 ) ���� ����� ����� ���� ����2.4.2013 ,���� ��� , ������ ��� ���� � �� �� ����� ��

���� �������31.3.2013 ����30.4.2013.(

����.5.201316 ����� ����� , ��Habas Star � � ��� ������� ���� �� ����-1.57 ���� ������

.(�� ��� � ���� ������ ���)

�� ��� ,����� �������� � ����� ����� �2.4.2013 '��) :������2013-01-022624(, 2.5.2013 '��)

:������2013-01-051835(� �- 16.5.2013 ������ '��)2013-01-062383( ,�� � �������� ������

����� �� ��.

8. �����15.3.3 ���� ������ ���� �����- (� �����) ���� �� ����� � �����15.6 - �������"

"�������) ������� ���� '��2 ���- ����� ����� �����-NSI(

�� �) ���� ����� �� ��� ��� �� ����� �� ������� �����4( ����� � ���� ������ ,2

������2013 .����� ��� �� ��� �� ��� "��� � ���"���� � ���� ���Habas Star

�� �) ���� ����� ����� �� �����4 ( �� ����� �� �� ���- 115.41%� ��� �� ��� ���� . -

"�������� ����" � �) ����� ��� �� ��� �� ��� ,120% � ��� ��� ���� ����� ,(60 ���

.� � �������� ���� �� ���� �� ������ ��� ������ ��� �� ���� ��� �����

���� � ��� �� ��� ,����� ������2.4.2013 ��) ' :������2013-01-022966( , �� ������ ��

����� �� �� ������.

9. �����19 ���� ������ ���� �����- ������� ������

�. ����22 ,������2013 ����� ��� ����� �����, ������ ������ ����� ��� ������� �����

���� ��� ���� ��� �� ��� �� ��� ������2011-2012 ������ ���� ����" ��

������ "� ������"�� ,������ ��� -1999������ ��� . ���� ���18 ,������2013 ������

��� ������ ���� ���� �������-���� ��� ����� ���� ���� ,����� ����� ���� �

������ � �������� �� ����� ����. ,�� � ���� ������ ��� �� � ��� ����� ����

.����� ����12.5.2013 ���� �� �� ��� ��� � ��� ����� � ���� ��� �� ���� ��� ����

����� � ����������� ���� ���� ������ ������ ����� ���� ���� �15.7.2013 ;

���� � ��� ,������� ����� ������ ���� ����7.9.2013, ���� �� ���� �� ���

����� ������ ,����� ������ ����� ���� ����� ���� � �� � ��� �� .���� ���� �� ,

.����� ���� ���� ������ ���� ��� ��� ���� ������� ����� �� ���� �� ,��

- 6 -

���� ����� � � ��� �� ��� ,����� ������23.4.2013 ) '�� :������2013-01-042601( ���

�����7.� . ���� ����� � ����� �� �31 ,����2013, ����� �� �� ������ ��� ������ �� .

�. ����28 ,������2013 ����� ��� ����� ����� , ,������� ������ ������ ����� ��� �����

�"��� ,��� ����� ��� ������ ����� ���� �����-1968 ����� ����� ��������� , ��

����� ���� � ��� �� �� ����� ������ � ���� ������ � � ��)Habas Star ( � ������ ������

�2012 – �� ��� �� ������ �� ������ ���������� ������� � ������ ����� ���� )�� �

4( .������ ���� ������ ���� ���� ������� ������ ���� ���� ���17 ,������2013 �� � �

�� �) ��� ������ ����� ����� ����� ���4����� � ( �� �) ���� ����� ���� �� ���)4 (

���� ����� �1 ,��������2012 ���� ��28 ,����2013 ����� ����� ��� ,����� � ,(

�� � ���� .����� �"��� ������ ���� ����� � �������� ,�� ��� �� � ��� �����

������� ����� ���� .����� ���� ����� �� ���� ���

����� ����� � ��� ��� ���� ��� ,����� ������25.4.2013 :������ '��)2013-01-044938 (

�- 28.4.2013 :������)2013-01-047014( ����� ���7.� . ���� ����� � ����� �� �31 ,����

2013����� ��� ������ �� ,����� �� �� �.

10. ����3 ,������2013 ,��� �� �� ����� ����� ) ����� ��� ����2005 ������ ����� ���� ,�"�� (

,��� ���� �� ,�� ����� ����� ��� ����� � ��������� � �"�� � ���� ����� �� � ���� ��

���� ������ �� �� ��� �� ������ ������ ��� �� ���� �� 1 ,������2013 ���� ������

30 ,����2013 �� � ��� �������� - 500,000 .�" ���� ����� � � ��� �� ��� ,����� ������

4.4.2013 :������ '��)2013-01-025882(.����� �� �� ������ �� ������ �� ,

����8 ,������2013 '��� ,����� � �������� ����� �"��� � ����� ���� �� ����� ��� ��

���� ��� ����� ���� �� ,���� �� 7 ,�����2013. ���� ����� � � ��� �� ��� ,����� ������

8.4.2013 :������ '��)2013-01-028993����� �� �� ������ �� ������ �� ,(.

����18 ,������2013 ����� ����� � ������ � ��� � ,����� �"�� ���� �� ������ ���� ���

(����� ������� ���� �������) ����� ��� ��. ���� ����� � � ��� �� ��� ,����� ������

18.4.2013 :������ '��)2013-01-038749.����� �� �� ������ �� ������ �� ,( ����� ������

����� ��� ����� ����� ��������� ��������� ����� �� ��9 ���� ����� � ������� ���� �

31.3.2013.

����13 ,����2013 ���� ���� ���� ,����� � ������ ������ ���� , � �� ������

��������� � ���� ,��� ���� �������� ������ ����� ������ ��) ��� ���� ��������

����� ����� ���� � ������ �� ����� ����� ���� ��� ����, �� ����� ����� �����

� ���� ��� ���( ������ ��� ������ ��/� ����� ���� �� ��/�� ����� � ����� ��//��� �

����� ����, ,�� ������ ��������� ���, � �������, ���� ���15 ,������2013 .

����� ����� � ��� ��� ���� ��� ,����� ������7.4.2013 :������ '��)2013-01-028624� ( -

13.5.2013 :������)2013-01-0611084.����� �� �� ������ ��� ������ �� ,(

- 7 -

27 ��� 2013

����� ) ������ �1960 (�"�

������� ���� ����� ��� ����:

��� ������������� � �"�� ,

����� �������� �"�� ,

�������� ��� ������� �

���������� ������� ������ ��� ��������31 ��� 2013

��������� ��� ) �����1960����) �"�� (: "�����(" ���� ���� ���� ����� ����� �� ��������� � �� � ��� ��� ����� ���� ���� ������ ����� ����� ����) �� �� ���� ������ " �������� (" ������

�� �� ��� � ����� ���� ������31 ���� 2013 " :����)����� �� �(" , ��� ������� �����48 � ���� (�� ���� �������� ���� ) ��� ����� �"�- 1970 " :����)���� ���� �(".

�� �� ������ �������� ���� ����� ������� ������� ����� ������� ������ ����31 ���� 2013 :����)"���� � �������(".

) ��������� ���� ���� ���� ����� ���� ������� ���� �IFRS����� ������ .(, ��� �� ����� �����2 �- 3 .������� ���� �

1. ����� ��������� ��� �� ������ �������� � �������"� ���" ���� 12 ����2013 � ���� ����� ���� �� �� �� ���� ��� �� �� ����� ����� ("���� � ���" :����)�

� � ���������� ��� ���2013 ,�� ���� �N.V. NSI ,���� ����� ���� ���� ������� ����� � �- 20.54% �� � � ������ " :����)NSI ������� ������� ����� �������� ����� ����� ���� ,("

,���� ���� ���� ��� ��� ���� .�� ������ ������ ������ ���� � ���� � ��� ��� �� ������� � ������� ������ �� ���� �� ����� �� ������� ���� ���� ����� ���� � ����NSI, ��� ���

� ������ ���� � ���� ��� �� ���� ,������� �NSI ��� ����� ����� ���� ����� ���� ��� .��� ����� ������ ������ ����� ���� ����

�� ��� �� ��� ,����� ���� �� � ���� ������ ������ ������ ������� ,��� �� � �������� ����� ������ ��� �� ���� ����� � ������� ���� ����� �� � ����� ������ ����� ����� �12 �- 4 �������

������� ��� �� ���2013 ���� ����� �� �� �� �� ���� ������ ����� ����� ��� ,����� ����� ..��������� ����� ���� ����� ������ ��� ����� �� ����� ����� ������

���� ����� ���� ,����� ��� �13 ���� 2013 ��� �� ���� ����� ������ ����� �������� ��� ��12 � - 4 ���� �� ,�� ����� ������ ����� ������� ������ ������ ���� �� ,���� ��� ,����� ������� ���� ,

����� �� ������ ��� �� ��� �� ,��������� ��� ����� ��� ��� ������� ��� ������ �� ������� �� ��� ���� ��� ���� , ��� ����� ��� ������ ����� ����� ,����� ������� ���� ������ ��

������ �� ��������� ��� ������ ����� ������� �� ��� .�� �� ������� ���� ����� ������� �����) ������ ����� ��� ���� ���� �� ���� ����� �����Margin Call���� ,( ������� ����� �� ��� ����

�����4 ����� ����� ����� ���� ��������� ��� .���� ������ ����� �� ���� ����� ��� ����� ��� ��� .� ;������ ����� �� ����� ����� ��� �� �� ���� .� :���� � ���� �� ������ ���� ���14 ���

��� ����� �� �� �� ����� ����� ������ ���� ����� ��� � �� ���� .� ;������ ����� �� ������ �� ��.���� ��� � � �� ���� �����

����� ������ ����� ���� ��� �� 12 �- 4 ,������� ���� 18 ���� 2013 ,���� ����� ��� ��� ��� �� ����� ���� ,�� ����� ����� � �� ����� �� ���� ��� ����� ��� �������� ��� ���� ���� ����� ����� .("������" :����)

����� ����� �� � ������� ����� ����� ����� �� ������ ������ �� ������ �������� � ������ ������ �� � ����� �� � ��� ���� ����� ,��������� ��� �� ���� � ����� ,�� ����� ��������

�������� ����� ���� �� � ���� ����� �� ����� �� ����� ������ ����� ���� ����� .����� �� ��� ������1 ,�6, 7 �- 9 ������� ���� �.

����13 ����2013 �� �) ���� ������ ���� �� �� �� ����� �����12 � ���� ���� �� � ����� � ( ������ ��� ����� ��� �� �) ��� ����� �12 ���� ������ ����� ��� �� ��� ,(31 ����2013 ���� ,17

����2013. ����19 ����2013������� , ���� � � �� ��� ����� ������ ����� ���� ������ ,����� ,����� ����

������� ������ �������� ����� ���� ����������� �������� �� � ���� ����18 ����2013 , ������ ���� ������� ������� �� ����� ���� ����� ������ ������ �� ��� �� ������ ���� �� � �����,

���� ����� ��� � ��� ����� (��� �� ��) ���� ����� ��� � � ������ ������ ���� �� � ����� ���� �� �) ��� ����� ������ ���� ���12 ( ������� ���� ����� � �� ��� ���� � ���� ����� , ��� ����� �

�� � �12 ���� �) ��� �� ���� �� ������26 �����2013.( �� �� ����� ���� ���� ��� �� ������ ��� �� ��� ��.

����� ������ ���� � ����� ,��� ��� ����� �������� � � ����� ,��� ���� 7 � ���� �������.

2

2. ���� ��

�. ����� ����

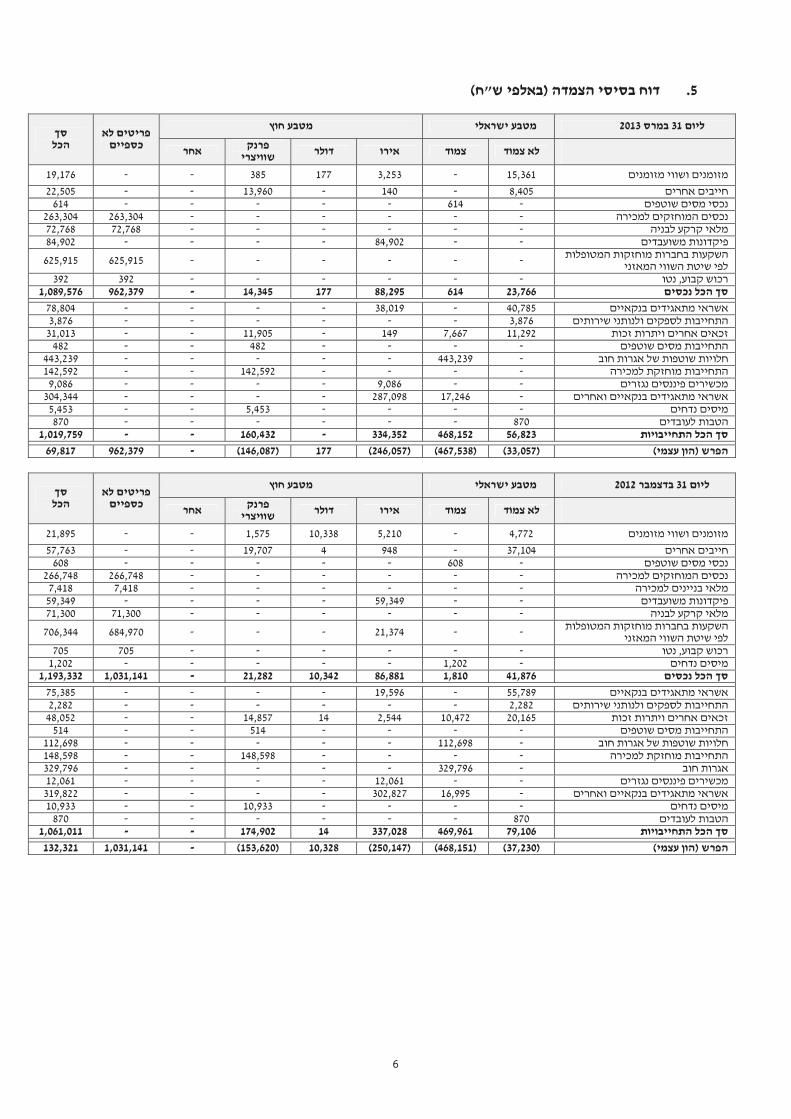

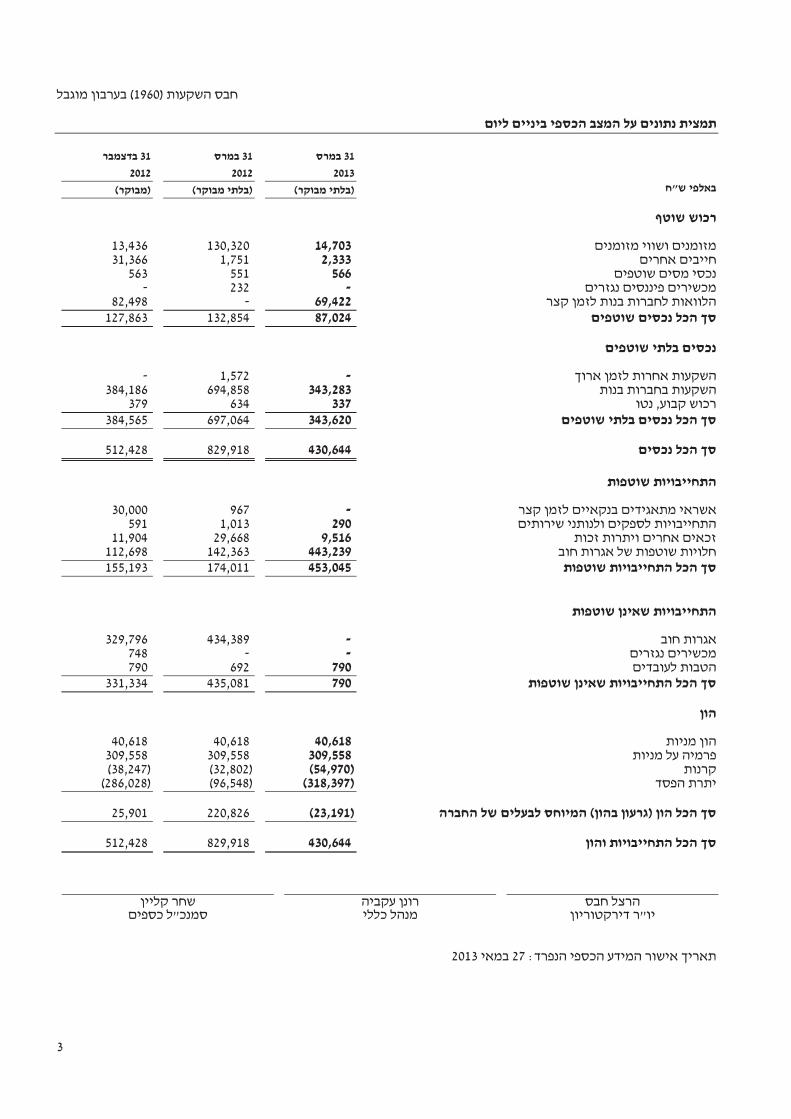

���� ������ � ����� ��31 ���� 2013 �������- 1,090 ������ ") �� � �� �����- 1,193 ������ " ����� 31 ���� �2012( .

���� ������ ���� �������� ������31 ���� 2012 ����� ������� ���31 ���� �2012 :���

����� ����� �������� ����- 3 ������ "� � � ���- 19 ������ ������) �" ��������", ����� ������ ������ ������ .(���� "

� � ��� ���� ������ ������ ����� �����- 35 ������ ����� ��� ,�" ������ � ��� ������30 ,�" ������

��� ����� ����� ������ ����� .���� ������ �����

����� � ���������� ���� ����� ������ � ������ ��� � ����� �������� �� �.

� ����� �� ����� � ��� �� ���� ������ ��� �- 26 ������ �"� � ���- 85 �" ������ ���� ��� ����������� .������ � �� ����� � ��� ����� , ���� ��� ������ ����5 �������� ���� .

������ ���� ������ � ��� ������� ������- 59 ������ � ���� ����� ����� ��� ,�" ������

� ����NSI � � ���- 21 �������" ���� �� ���)2.2 (���� , ��� ���� ����� � ������� �� � ����� � �����5.3% .�� � ������

. ����� ��������

���� ������ ���������� �� ��31 ���� 2013 � ������- 1,020 ������ �" )� � �� �����- 1,061 ������ "� ���� 31 ���� �2012(.

�������� ���������������� ���� ������31 ���� 2013 ����������������� � ���31 ���� �2012 :���

� � ��� ������ ����� �� ����� ����� ����� �����- 12 ������" ����� ��� ,� ����� ����� � ��� ��� �"��� ������� � �������� ����� � ������� ������� �������� ���� �������� �

������� � 5.3% �- 6.2% ������.

������ ����� �� ��� ,�� � ����� �� ������ �� � ���� ��� �� ����� � ��� ���� ��� ,���� � ����� ,������� �� ��� ������� ������ �� ����� ����� ������� �� ��� .� ,�� ���� ���� ����� � ��� ������

NSI � ������- Euronext NYSE Amsterdam �� � ������ ����� ������ ������� ���� ��� ���� ��� , �����NSI ���� � ������� ���� ����NSI (LtSV) � ���� ���31 ���� 2013 � ��� ������ ���� � ���

�- 18.2 .����� ���������� ����� ���� ������ � ,���� � ��� � �� �� ����� �� ���� ���� � ����- 18.7 .���� ������ ����� ������ ��� ����5 � ���� �������.

����� ������7 �� ������ ������ ����� ���� ��/� ������ ����� ������ ����� �� ����� ,������� ����

�� �) ��� ����� ������ �������4.� ��� ������ ���� ����� ��� ��� ����� ��� ��� ,( ����� ��� ,���� �� �) ���12 ����� � ���� �� � �� ����� ,� ��� ������ ���� ����� ��� ( ����� ����� ���� ���

,����� ����� .� ��� ������ � ���� .���� ��������� ��� ����� ���� ������������ ��� �� ����� ����� ������ ����� ���� ���7 ��.������� ����

� ��� ��� ������ ���������� ���� �� � � �� ������ ���� ����� ��� ��� ,����27 ���� 2013 , ������� ���� � ����- 126.

.� ����� �� ����

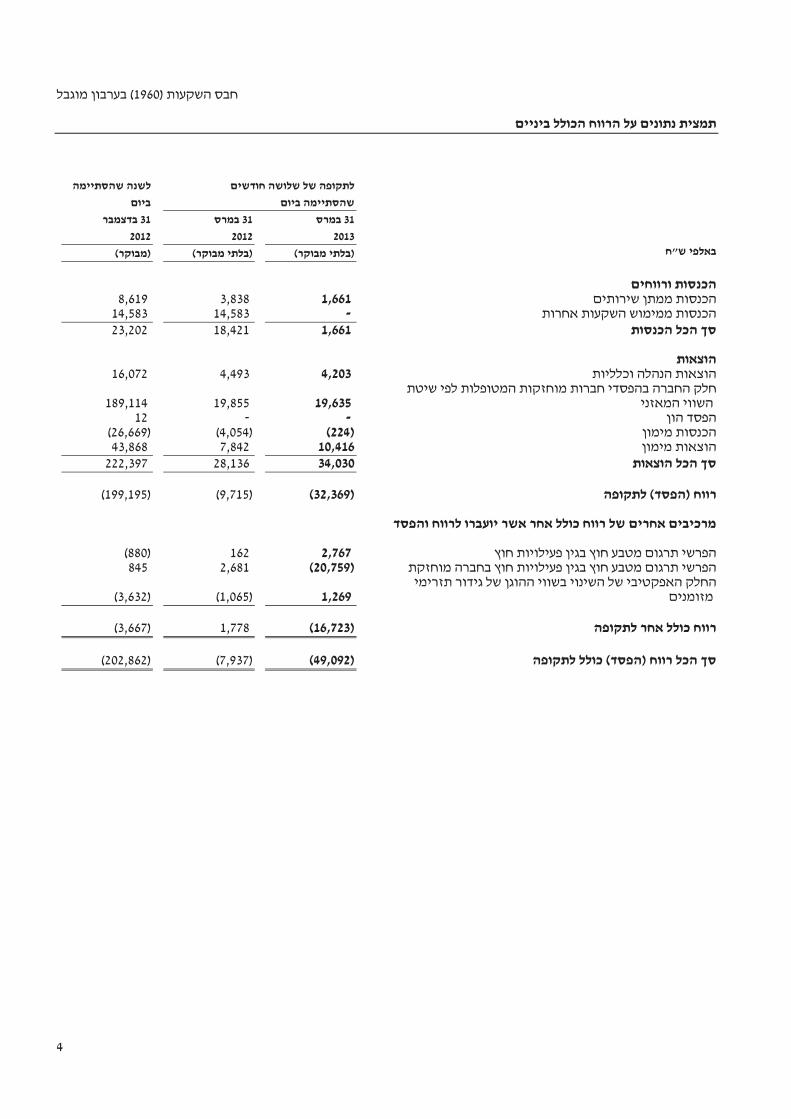

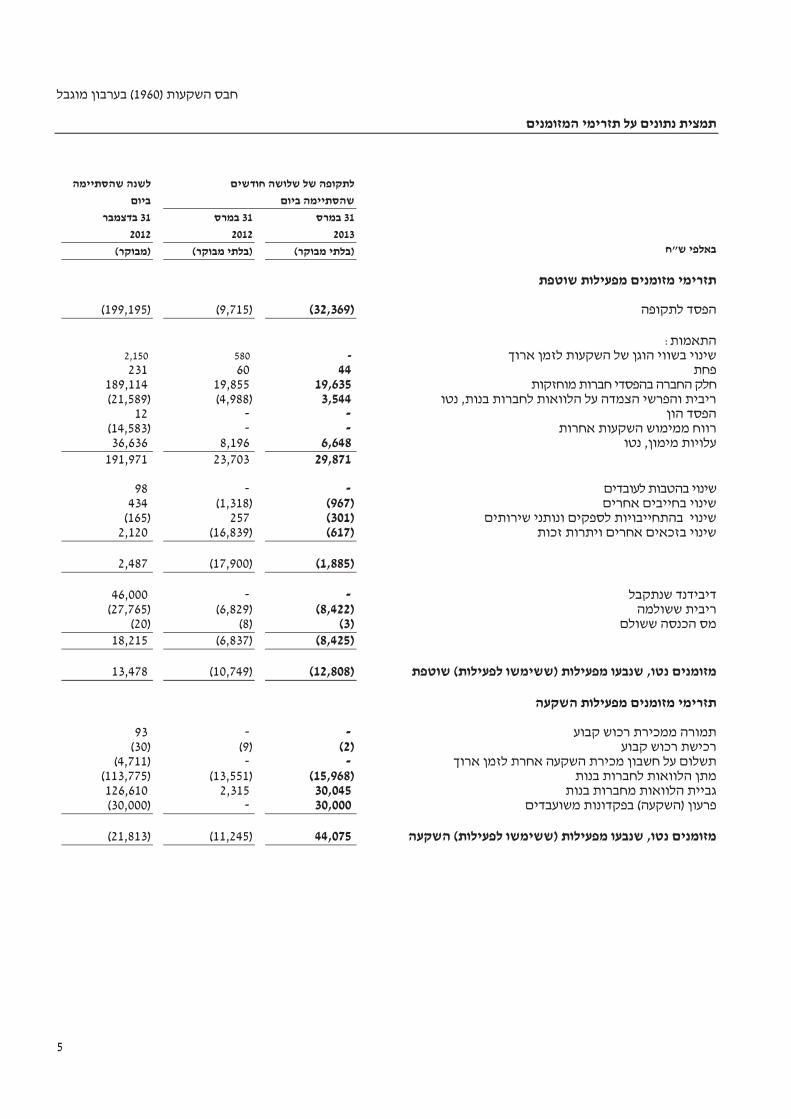

������ � ���� ���31 ���� 2013 � ������- 70 ������ ����� �" � �� �- 132 ������ ���� �"31 ���� �2012 . ���������� ����, ��� � �- 62 ������ "�, ��� �� ��� � ����� ������ ���� �� ������

� ������ ���) ������ ������"�(���� "��� .

3

.� ������� ������

1. ������

1.1 ����� �� � ����� �� � ������ ����� ������ ��� ����� �� � � ��� ��� �"� �- 3 ������ ������ .�"

����� ����� ��� ��� �������� � ��� ��� �"� �- 8 ������ " ������ .�� �2013 ��� ����� ������ ����� ���� ������ � ���� .����� ������ ����� ���� �"�

���� � ���� �2012.

1.2. ���� ������ ����� ��� � ����� ������ ������ ����������� ��� � ������ � ������Yoo Tel Aviv � ����- 12.5 ������ "�.

2. ������

2.1 ������� ���� ������ �������� ����� ������ ����� � ����� �������- 5.5 ������ ������ .�" ��� ������

�� �������� ����� ������ ������- 6.7 .�" ������ ������ ��� ,������� � �- 1.2 ������������ �� ���� ���� ����� ��� ��� ������� � ���� ����� ��� �" .������ ����� ����

������ ������ ,���� ��� ,�������� ����� ������� �������� �������� ����� �������� ���� ���� � ��� . ��� ����9 .������� ���� �

2.2 ������ ���� ���� ������� �����

�� � ������ � � ��� ������� ����� � ���� ���� �� ������ ���- 21 ������ .�" ������ ��� , ��� ������� ������� ���� ��� � � ��� ������� �����- 16 ������

.�" ����� ������ � ������ ����� ����� ��� ������NSI � ������ ������ .NSI (Direct result) �� ������- 13.4 ������ ����� ��� ������� .���������� �� ��� )Indirect

result( � ����- 34.3 ������ ����, ������� ���� ��� � ���� ����� ( ���� �� �� �����) �� ���� � ����� ����� �����(Swap). ��� � ������� ������ ��NSI ��������� ����

.�������

2.3 ��� �"� � ���� ���� � ���

� � ��� ��� ������ ��� �� � ������- 12 �"� � �� � ����� ����� � ���� �" ������ ���� ����Dietikon .�����

2.4 ������� ���� ���� � ���

� � ��� ��� ������ ��� �� � ������- 3.2 ����� ����� � ���� �" ������ � �����

�� ������ .������ ������ ����� �9 .������� ���� � ������ �

2.5 ������ ������������� ,

�� � ������ ������������ ����� ����������� �� ��� ����� �- 8 ������ �" ������ . ���������� ���� ������ ����� ��� ��� ������� ������ ������ ������ �������

������� ������ � � ��� ����� ������ � �� � ������ �����- 5 �" ������. ������ ������ ,������ ����� ��� �������� ��� ������ ������ ���� � ��� ������

������� ����� ����� ��� ����� ���� ������.��� ��� ����� ���� ������ ���� ���� �� ��� .����� ����� ������ � ����� ����� �����

3. (����) ����� ����

���� � � ��� �� � ������ ����� ���� �����- 21 ����� ��� �" ������ ���� ����� ����� ���� ������ ������� � ��� ���� ����� ����� ����� ��� ������� ������ .- 2 ��� �" ������

���� ��� ���� ����� ����� �����.��� ������ �� ����� �� � ������ ����� ���� ��- 63 � .�" ������- 49 ������ ������� �� ���� �" ������

�� ����� �- 14 ������� ������� �" ������.���� ���� ���

4

.� ������, ���� ������ ������� ������

�� � ������ � �� ���� �����- 14 ������ " �� ������� ����� �� ������� ������ .����2012 �� ��� �� �����- 16 ������ �"�������� ����� .

������ ���� � � ��� ����� �� ��� �� ������ ������ �� ����- 2.5 �" ������ � ����� �������� ������� ���� Yoo Tel Aviv � � ���- 3 �" ������. � � ��� ����� ����� ������� ��� , ��- 13

� � ��� ������� ���� ������ ����� ,�" ������- 5.5 �" ������� � ��� ������ ����� ����� ����� ��������".

� � ������ �� ��� ����2012 ��� ����� �� ��� �� ������ ������ �� ���� ������ ����

� �- 7 �� ������� ���� ����� ��������� �" ����Yoo Tel Aviv � � ���- 4 �� ��� , �� .�" ���� �������� � ��� ����� �����- 13 ��� � ��� ������� ���� ������ ����� ,�" ����- 7 �� �" ����

� � ��� ������ ����� ����� ������- 5 �� .�" ����

���� ������� ��� ������� ����� � ����� �� �����- 8 ������ "� ����� �- 2 �������" ��� ���� ������� ������� ������� �2012. �� � ������ ���������� ����� ��� ���� ����� �����

� � ���- 9 � � � ���) �" ������- 30 � ��� ����� ���� �" ���������� � �� ����� LtSV ���� , �30 � � ����� ����� ������ ������ ����� ����� �" ������- 8 �" ������ ������ �� �� ����

���� ���� ���� (�����. � � ������ �� ��� ����2012 ������� ��� ����������� ��� � ��� ����� ���� ������

���� � �� ����� LtSV � � ��� ,- 11 �� �" ����� ��� ������ ����� ����� �"� ��� ������ ��� �� ����� ������- 10 ��.�" ����

�� � ������� ���� �����- 3 ������ " �� ����������� �� ����� ������� ����� �������� ������, �����53 ��� ������� ������ �" ������ � ����� ��� ����� �� �) ��� �����4( � � ���- 55 ������

�".

3. ����� ����� ��� ������ ����NSI

�� � ���� � ���� ����� ����� ��� ������ ��� ����� �� �� �� ���� ���� ����� ������ ����� ���� ����� ����� �� �8 �������� ���� ) ��� ����� ����� ���� ���� (� �"1970 .���� ����� ������

�� � ����� ����:

��� ������ ���� ����� ������NSI ����� ����� ���� 31.3.2013 ��� �� ������, ���� ������ ��� ��� ����

,������� ��� ����� ,�������� ������� ���� ������ ����� ���� ��� �� ������� ��� ��

����

132.6 ������ ���� ,��� ��� � 618.1 ������ �"

��� �� ������ ��� ����� ������ 132.6 ������ � ��� ��� ,���� 618.1 ������ �" ����� ������ ������� � ���� � ������ ���� � � �� �����Professor Israel Shaked.

Professor Shaked��� ����� ���� ���The Michael-Shaked Group ������ ,����� ,����� ��� � ����� ������ ���������� �- 30 � ����� .

� ���� ������ ������ ,�������� ���� ���� �� , ,��� ���� �� ���� ��� ����� ������� ������ �� ���� ������ ,�������� ������ ��� ������-

Securities Exchange Commission (SEC), the Internal Revenue Service (IRS), the Federal Deposit Insurance Corporation (FDIC), the Department of Labor (DOL), and the Pension Benefit Guarantee

Corporation (PBGC) .Professor Shaked ���� �������� �� ����� ������ �� �����- Boston University School of Management ���� ��� ���� ����� .

.����� � � �� ����� �������� ���� ������ ��� �� ��� ����� � �� ����� ���� ��� �- NAV ������� ������ ���� ���� � ���� ���� ��������

����� ����� ���� ����� ���� �� ������ ,����� � ��� ������� ������

�� ����� ������� ������ ���� ������� ��� �������

� ����� ��� ���� ��� ����� �� �� ������- Dietikon ��� ������ ��� ����� �� �� �� ���� ,�����

���� ��� ,������� ���� � ���� � ���� ����� �����3 .����� ���� ����� ��� ��� ��

5

4. ������ ����� ��� ������� ����

.� ����� ��� ������ ������ ������ ������NSI ����

���� ����� ������� � ��� ��� ,���� ��� ,����� ���� ����� ����� �� �����NSI ���� ��� ,������1.1 ����� ����1.������� ���� � �

. ������� ������ �������

����� ������� ����� ������� ���� ��� ����� �"��� ������ � ������� ,������� ������ ����� ,����� ������ ������� ������ ���� ���� ������ ������ �� ��� .������ ����� ���

�� ������ ����� ������ ��� ,������� ������ ������ �� �������� ����� ���� ����� .����� � �� �������� �"� � .������� �"� � ����� � �� ��� ����� � �� �� ������� ������� ������� ����

� ������� ����� ������� ,���� ��� ,���� ����� �� �� ������ ���� ,����� ����� ����� ����� ,���� .���� ���� ���� ������ ����� ,���������� �� ���� �� ������� ����� ����� � ��

��� ���� ��� ,����� ����� ������ ,�� �� � � �� ������ ������ ������ ���� ����� � .���� � ������ ������������ � �� ������ �����.����� � � � ������� ����� � ����� ,���� � ����� ���� ���

����� ����� ���� ������� ����� ����� � ��������� �� ���� ������ ����� ,���� �� ,���� ���.����� �������� � ����� ���� ����

�. ��������� ���� ������

��� ��� ����� ����� ������ ������� ��� ��� ������� �� � ����) �����48% ��� �����

�� ����� ���� ����� ��� ���� ���31 ���� 2013 �������� ����� ����� ����� ,�� ����� ��� .( . ���� ������ � �������� �� ����� ����� ����� �����

����� ��� ,������ ����� �� ��� ������ ������� ������ ������� ������ ���� ��� ������ ������� ������� �� ��� .� ��� ��������� ����� �� ������������� ���� �� �� ����� ����� ������

���� ����� ������ ������ � ����� ���� �� . �. ���� ��� ������

������� ������� �� ��� ��� ��� ��� ������ ����� ��� �"��� ������ ������ . �� �� ������ ����� � ���� .������ �� ���� ������ ���� ���� �� ��� ��������34% ���� ������ �� ����� ����� ���

���� ����� ��� ������31 ���� 2013 � ����� ����� ���14% ���� ������ �� ����� ����� ��� ���� ����� ��� ������31 ���� 2013 ��������� ���� .���� ������ ������ ������� ������� ,���

,����� ����� � ������� ���� ������ ����� ������ ������ �� ��� ������� ����� ����� . ����� � ��� ��� ����� ����� �� ���� ��� ������ � ������������ ����� ������ ���� ����� ���� ��

������ ����� � ������� ���� ������ ����� �� ��� ����� ����� ,���� .(��� ������ � ����� ���) �� ��� ����� ���� ����� ��� ����� �� �� ����� ������ .����� ������ ������� ������� �����

,����� ������ ������� ��������� ���� 8 �� ��� ������� ���� ��� 27 ������� ���� � ����� ��2012.

����� ����� ,��� ����� ����� ������ ���� � ����� ����, ���� �� ���� ����� �� ������ ����

������ �������- �� ��������� � �� � ����� ����� ��� ���2012.

6

5. ("� ����) ����� ���� ��

���� 31 ��� 2013��� ��������� �� ������ ��

�������� ���

�� ������������ ��������

���������

������ ���� ������15,361 -3,253 177385--19,176

������ ����� 8,405-140-13,960--22,505��� ���� ����� - 614 - - - - - 614

���� �������� ������ - - - - - - 263,304 263,304 ���� ���� ����------72,76872,768

��� ��� �� ���� - - 84,902 - - - - 84,902 ����� ������ ������� ��������

����� ���� ��� ��� --- ---625,915625,915

��� ���� ,��------392392�� ��� �����23,76661488,29517714,345-962,3791,089,576

���� �� ����� ������40,785-38,019----78,804 �������� ������ ����� ������ 3,876------3,876

����� ���� ������ ����� 11,2927,667149-11,905--31,013�������� ���� ����� - - - - 482 - - 482

������ ����� � ����� ��� - 443,239 - - - - - 443,239 �������� ������ ������ - - - - 142,592 - - 142,592

����� ����� ������ - - 9,086 - - - - 9,086 ���� �� ����� ������ ������ -17,246287,098 ----304,344����� ��� ----5,453--5,453����� �� ���� 870------870

�� ��� �������� 56,823468,152334,352-160,432--1,019,759

���� ��)����( )33,057()467,538()246,057(177)146,087(-962,37969,817

���� 31 ���� 2012��� ��������� �� ������ ��

�������� ���

�� ������������ ��������

���������

������ ���� ������4,772 -5,210 10,3381,575--21,895

������ ����� 37,104-948419,707--57,763��� ���� ����� - 608 - - - - - 608

���� �������� ������ - - - - - - 266,748 266,748 ���� ����� ������ - - - - - - 7,418 7,418

��� ��� �� ���� - - 59,349 - - - - 59,349 ���� ���� ����------71,30071,300

����� ������ ������� ������������� ���� ��� ���

--21,374 ---684,970706,344

��� ���� ,��------705705����� ��� -1,202-----1,202

�� ��� �����41,8761,81086,88110,34221,282-1,031,1411,193,332

���� �� ����� ������55,789-19,596----75,385 �������� ������ ����� ������ 2,282------2,282

����� ���� ������ ����� 20,16510,4722,5441414,857--48,052�������� ���� ����� - - - - 514 - - 514

������ ����� � ����� ��� - 112,698 - - - - - 112,698 �������� ������ ������ - - - - 148,598 - - 148,598

����� ��� - 329,796 - - - - - 329,796 ������ ����� ����� - - 12,061 - - - - 12,061

���� �� ����� ������ ������ -16,995302,827 ----319,822����� ��� ----10,933--10,933����� �� ���� 870------870

�� ��� �������� 79,106469,961337,02814174,902--1,061,011

���� ��)����( )37,230()468,151()250,147(10,328)153,620(-1,031,141132,321

7

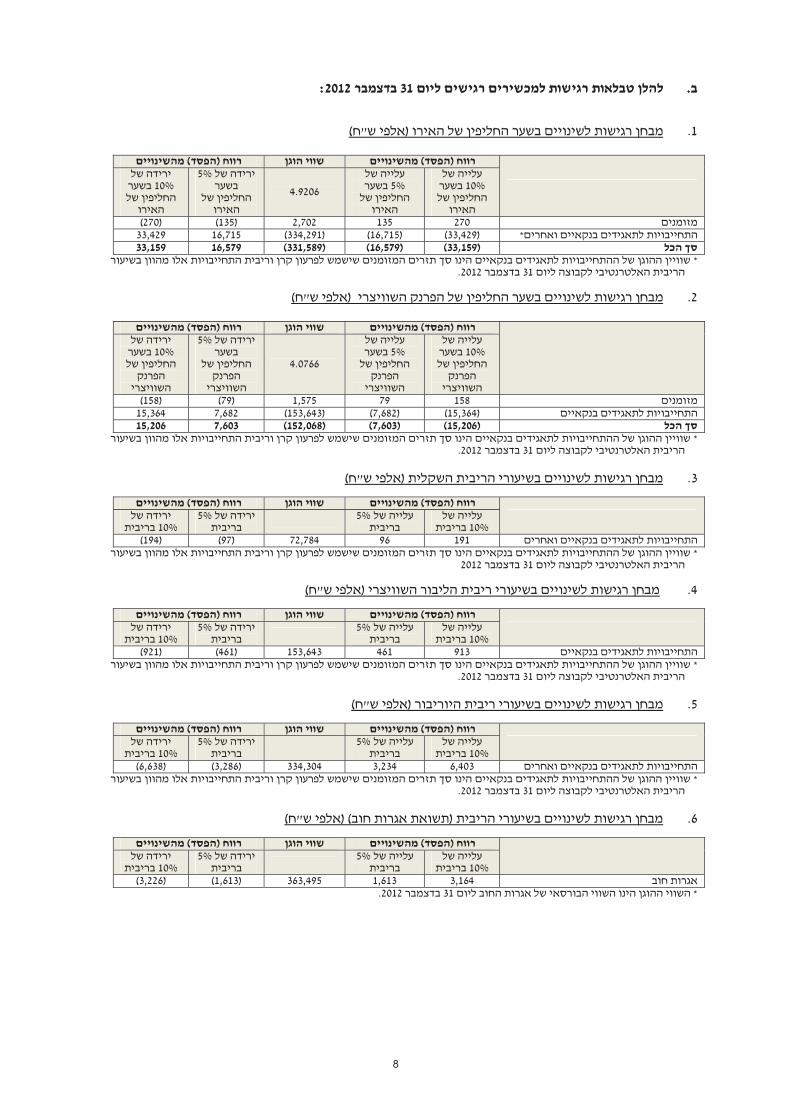

6. :������ ���

.� ���� ������ �������� ������ ����� ���31 ��� 2013: 1. ����) ����� � ������� ��� ������ ����� ����"(�

��������� (����) ��� ��� ���� ��������� (����) ��� � �����

10% ��� � �������

�����

� ����� 5% ���

� ������������

4.6612

� � ���5% ���

� ������������

� � ���10% ���

� ������������

������ 325 163 3,253 )163( )325( *������ ������ �� ����� ���������� )31,719( )15,859( )317,185( 15,859 31,719

��� �� )31,393( )15,697( )313,932( 15,697 31,393 ����� ����� ��� ���������� ������ ��� ������ �� ������� ����� �� ��� ������ �� ����� ����������� � ����� ����� *

���� ������ ��������� ������31 ���� 2013. 2. ���� � ������� ��� ������ ����� ���� ����) �������"(�

��������� (����) ��� ��� ���� ��������� (����) ��� � �����

10% ��� � �������

�����������

� ����� 5% ���

� ������� ����

�������

3.8247

� � ���5% ���

� ������� ����

�������

� � ���10% ���

� ������� ����

������� ������ 39 19 385 )19( )39(

������ �� ����� ���������� )14,222( )7,111( )142,218( 7,111 14,222 ��� �� )14,183( )7,092( )141,833( 7,092 14,183

������ �� ������� ����� �� ��� ������ �� ����� ����������� � ����� ����� * ����� ����� ��� ���������� ������ ������� ������ ��������� ������ 31 ���� 2013.

3. ����) ����� ������ ������ ������ ����� ����"(�

��������� (����) ��� ��� ���� ��������� (����) ���

� �����10% ������

� �����5% ������

� � ���5% ������

� � ���10% ������

������ ������ �� ����� ���������� 170 85 43,031 )86( )173( ����� ����� ��� ���������� ������ ��� ������ �� ������� ����� �� ��� ������ �� ����� ����������� � ����� ����� *

���� ������ ��������� ������31 ���� 2013 4. ����) ������� ������ ����� ������ ������ ����� ����"(�

��������� (����) ��� ��� ���� ��������� (����) ���

� �����10% ������

� �����5% ������

� � ���5% ������

� � ���10% ������

������ �� ����� ���������� 880 440 142,218 )440( )884( ����� ����� ��� ���������� ������ ��� ������ �� ������� ����� �� ��� ������ �� ����� ����������� � ����� ����� *

���� ������ ��������� ������31 ���� 2013. 5. ����) �������� ����� ������ ������ ����� ����"(�

��������� (����) ��� ��� ���� ��������� (����) ���

� �����10% ������

� �����5% ������

� � ���5% ������

� � ���10% ������

������ ������ �� ����� ���������� 5,886 2,966 317,185 )3,024( )6,106( ����� ����� ��� ���������� ������ ��� ������ �� ������� ����� �� ��� ������ �� ����� ����������� � ����� ����� *

���� ������ ��������� ������31 ���� 2013. 6. ����) (��� ����� ����) ������ ������ ������ ����� ����"(�

(����) ������������ ��� ���� ��������� (����) ���

� �����10% ������

� �����5% ������

� � ���5% ������

� � ���10% ������

��� ����� 1,799 917 206,664 )917( )1,834( ���� ���� ����� � ������� ���� ��� ����� ���� *31 ���� 2013.

8

. ����� ��� ���� ������ �������� ������31 ����2012: 1. ����) ����� � ������� ��� ������ ����� ����"(�

��������� (����) ��� ��� ���� ��������� (����) ��� � �����

10% ��� � �������

�����

� ����� 5% ���

� ������������

4.9206

� � ���5% ���

� ������������

� � ���10% ���

� ������������

������ 270 135 2,702 )135( )270( *������ ������ �� ����� ���������� )33,429( )16,715( )334,291( 16,715 33,429

��� �� )33,159( )16,579( )331,589( 16,579 33,159 ����� ����� ��� ���������� ������ ��� ������ �� ������� ����� �� ��� ������ �� ����� ����������� � ����� ����� *

���� ������ ��������� ������31 ����� 2012. 2. ����) ������� ���� � ������� ��� ������ ����� ����"(�

(����) ������������ ��� ���� ��������� (����) ��� � �����

10% ��� � �������

�����������

� ����� 5% ���

� ������� ����

�������

4.0766

� � ���5% ���

� ������� ����

�������

� � ���10% ���

� ������� ����

������� ������ 158 79 1,575 )79( )158(

������ �� ����� ���������� )15,364( )7,682( )153,643( 7,682 15,364 ��� �� )15,206( )7,603( )152,068( 7,603 15,206

������ �� ������� ����� �� ��� ������ �� ����� ����������� � ����� ����� * ����� ����� ��� ���������� ������ ������� ������ ��������� ������ 31 ����� 2012.

3. ����) ����� ������ ������ ������ ����� ����"(�

��������� (����) ��� ��� ���� ��������� (����) ���

� �����10% ������

� �����5% ������

� � ���5% ������

� � ���10% ������

������ ������ �� ����� ���������� 191 96 72,784 )97( )194( ����� ����� ��� ���������� ������ ��� ������ �� ������� ����� �� ��� ������ �� ����� ����������� � ����� ����� *

���� ������ ��������� ������31 ���� �2012 4. ����) ������� ������ ����� ������ ������ ����� ����"(�

��������� (����) ��� ��� ���� ��������� (����) ���

� �����10% ������

� �����5% ������

� � ���5% ������

� � ���10% ������

������ �� ����� ���������� 913 461 153,643 )461( )921( ����� ����� ��� ���������� ������ ��� ������ �� ������� ����� �� ��� ������ �� ����� ����������� � ����� ����� *

���� ������ ��������� ������31 ����� 2012. 5. ����) �������� ����� ������ ������ ����� ����"(�

��������� (����) ��� ��� ���� ��������� (����) ���

� �����10% ������

� �����5% ������

� � ���5% ������

� � ���10% ������

������ ������ �� ����� ���������� 6,403 3,234 334,304 )3,286( )6,638( ����� ����� ��� ���������� ������ ��� ������ �� ������� ����� �� ��� ������ �� ����� ����������� � ����� ����� *

���� ������ ��������� ������31 ����� 2012. 6. ����) (��� ����� ����) ������ ������ ������ ����� ����"(�

(����) ������������ ��� ���� ��������� (����) ���

� �����10% ������

� �����5% ������

� � ���5% ������

� � ���10% ������

��� ����� 3,164 1,613 363,495 )1,613( )3,226( ���� ���� ����� � ������� ���� ��� ����� ���� *31 ���� �2012.

9

7. ���������������������

��������� �������������� ������������������� .������������������ � ������� � �������� ���������� � ,������������� � ��������������� ��������� �, ���� ��� ��� ��� ��� ����� ��������� � ����� ��� �� ���� ��� ��� .��� �����,�������������� �� ����� ������

��/� ����� �"�����"� ������� ����� � ��� ���� �� ������� ������������������ � ������� ���������������� �� ," :�� ����� ����) ����� � ������� ���� � ����� � ��� .� ��� ,("

�� ���� �� ���� ������ .����� �� � ����� ������ ���� ���� ���� ����� ,��������� � � � ������ ����� ,����� � ����� ����� ���� ����� ,����� �� � ����� ����� ���� ��� ��� ,� ���

.����� �� � ��� ��������� � ������ �� � ���

.����� � ������� � �� ��� ,� ����� �:�� � ��� ���� .������ ���� �������� ��� � ��� ���� ���� ���� ��- .� ��� �"��� ����� ������

����� �� ���� ��- .����� ������ ���� ���� ��- .������

������ ������ ������� ���� ��� � ��� ���� �� ��� ��� �� �� �������3 ����) ������ �����

� ������ ������� ��� ������ � ������ �"��� ,(������� ����� ��� ������ �� �����- 2005 ������ . ������ ����� ,���������� ����� �� ����� ����� ��� �� ����� � ������� �� �2012 ������ .

������ ���� ������ ����� ��� ������ ����� ,������� ��� � ����� ����� ��� ���� ,���� �" �������� ���� ���� ���� ���� .������� ������ �� ������ ������ ���� ���� ����� ,����� ������

������ ,��������� � ���� ���� ,� ��� � ����� ������ �������� ,��� ������ �������� ���������� �������� � .���� � ������ ������ ����� ������� �������� ���� ������ �������� �

�������� �������������� ���������� �������������� ���� � ������� .������� � ����� ,��������������������� �������� .�� ������ ���� ��� ��������� � ���� ���� ��������

.������ ������ �� � ���� ���� ������31 ����2013 :���� ������ ����� ��� ���� ���

.� " :����) ������� ���� � ����� � ��� ����� ��� ���� ("23 ���� 2013 ����� ���� ��� ��� �� ,

����� �� � �����, ��� ��� �� ����� � ������� ����� �� ,� ��� ���� � ���� ���� ��� ����� .����� � ����� ����� ���� ,����� �� ���� ��� ���� ���� �� ,���� ���� ,����� ����� ������

� �����, ���� ��� "���- ,� ���� �"�� ���� ����� .����� ������� ����� ����� ,���� ���,��������� � �"�� ,��� ���� �� �� ����� ,������ ,��� ���� �� �� ,����� �"�� ,����� ��� ��

���� ����� �� ������ �� ,����� �� ,���� �� ��� ����� � ������ �"��� ,����� ��� ������� �� ,���� ��� ,� ��� ��� ����� ����� .���� � � �� ����� ��� �� �� ����

������� ����� ��� ������ ������ ��� ���� � ������ ���� �� ,������� ���� � �������� � ������ ����� �������� . ���� �� ����� �� �� �� ����� ���� � � �� � ��� �� �� ,�� ���

,������ ����� � ���������� ����� �� ��� � � ��� � ������� �� � ������ ����� ��� ��2012. �� � �� ��� ����� ��������� � ����� � ��� ���� ����� ������ ������� .

���� ��������� � ����� ���� ������ ������23 ���� 2013.

.� ����� ��������� ������� ������� ��� 27 ���� 2013 , ������� ��������� � ,���� ��� ,�����.� ��� ������� ����� ���� ,��������� � ���� ��� ����� ���� ���� ����� � �����

��������� � �� ���� � ��� ����� �� ���� ����� ��������� ����� ����� ���� .������� � � ����� ������2013.

10

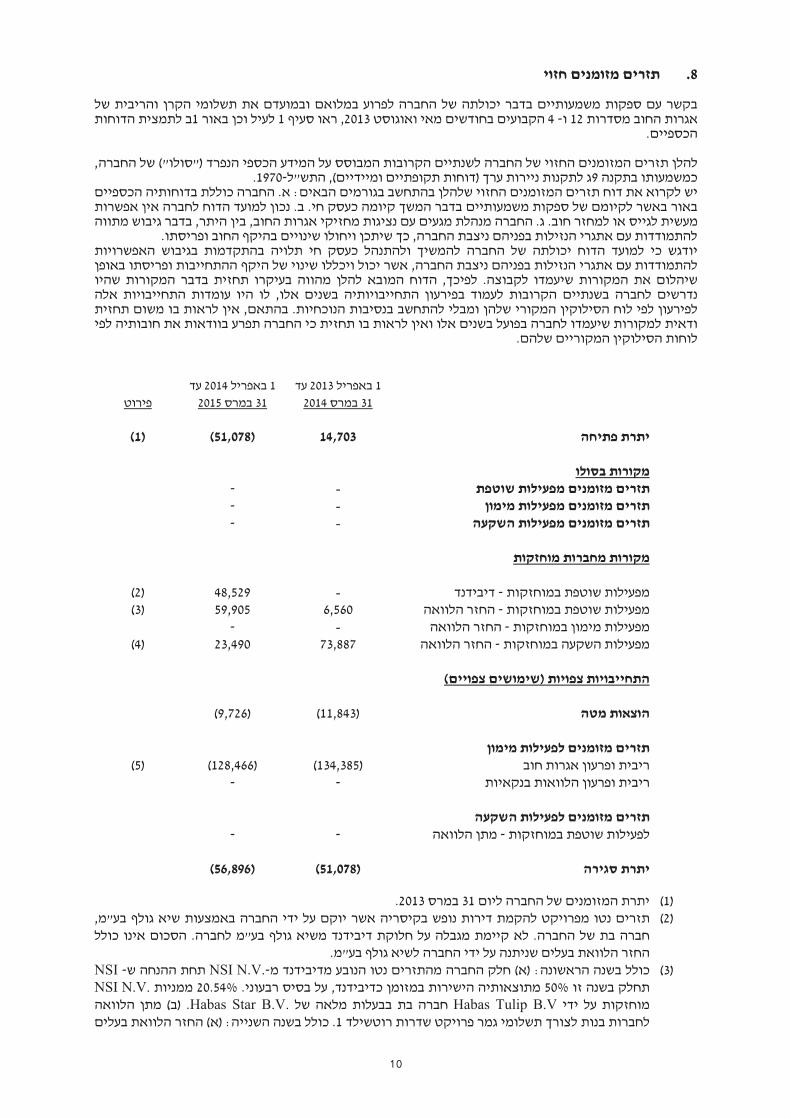

8. ��� ������� �����

����� �� ������ ����� �� � ����� ������ ����� ����� � ������ �� � ��������� � ������� ��� �� ���� �����12 �- 4 ������� ��� �� ��� �������2013 ���� ��� ,1 ��� ���� ����1 ���� � ������ �

�������.

� ����� � ����� ������� ����� ����������� ���� ,����� � ("����") ��� ����� � ��� �� ������ ���� �������9�"�� ,(��� ���� �������� ���� ) ��� ����� ����� �-1970 .

������� ������ � ����� ����� .� :����� ������� ����� ���� ����� ������� ����� �� �� ����� ��������� ����� � ������ ��� ���� ����� ��� ����� �� � ���� ��� .� .�� ���� ����� ��� �� �

���� ����� ������ ����� �� ����� ���� ����� .� .��� ����� �� ����� ����,���� ��� , ���� �� ������ ����� ���� ����� ������ ����� �� �� ����� , ����� ������ ���� ������� ���� ������� .

����� �� ���� ������ ����� ����� � ������ �� � ���� �� � �� �������� ����� ��� ��������� ���� ����� ������ ����� �� �� �����, ��� ��������� ��� ����� ��������� ������� �����

.������ � ��� ������� �� ����� ����� ���� ����� �� � ,����������� ��� ������� �� � ����� ����� ��� ������� ����� ����������� ������� ����� ��� ���������� �� ��� ��� �� ,��� ���

��� ������ �������� ��� ��� ������� ������� ������ ����� ����� ,����� . ����� ��� �� ����� ��� ��� ���� ����� � ��� ������� ��� ����� ����� �� ����� �� ����� ���� ���� ��� ��� ��� ������� ��

.��� �������� �������� �����

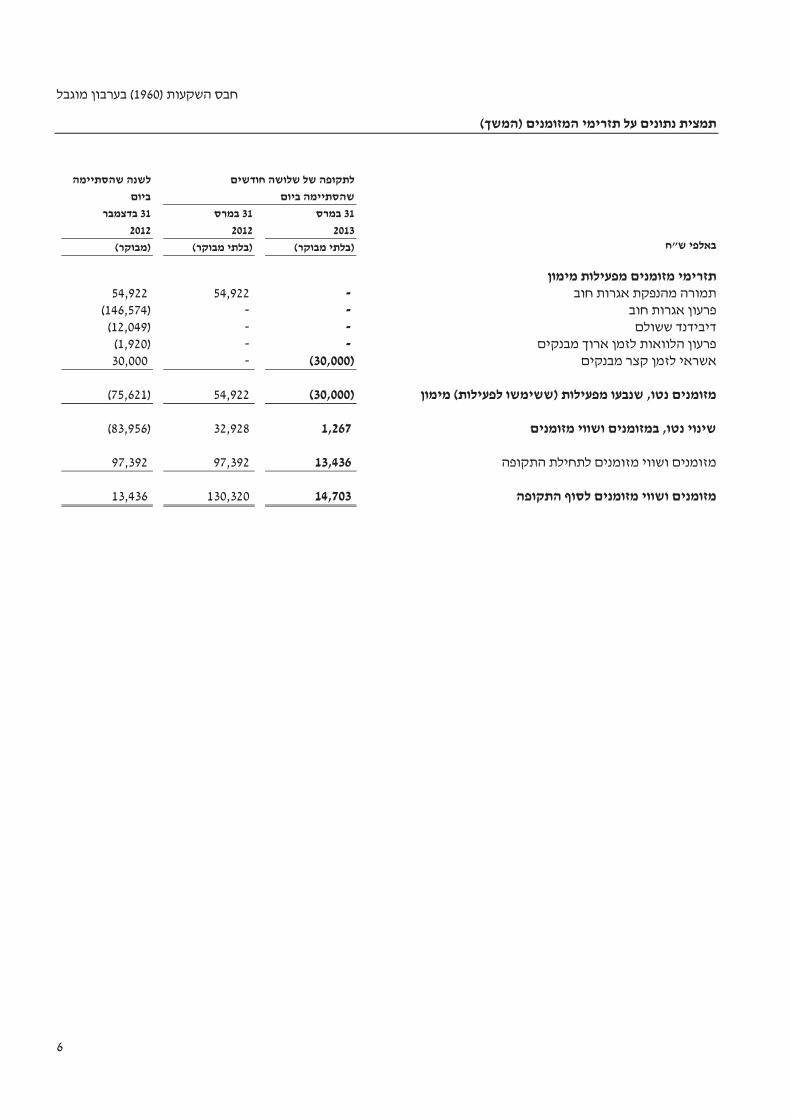

1 ������2013 �

31 ���� 4201

1 ������2014 �

31 ���� 5201

�����

���� ����

14,703

)51,078(

)1(

���� ������

����� ������� ������� ����� - - ���� ������� ������� ����� - -

����� ������� ������� ����� - -

������ ���� ������

�������� ���� �������- ��� - 48,529 )2( �������� ���� �������- ������ ���� 6,560 59,905 )3(

�������� ����� �������- ������ ���� - - �������� ���� �������- ������ ���� 73,887 23,490 )4(

(������ �������) ������ ��������

��� ������

)11,843(

)9,726(

���� ������� ������� �����

��� ����� ������ ����� )134,385( )128,466( )5( ������ ������� ������ ����� - -

���������� ������� �������

�������� ���� �������- ������ ��� - -

����� ����

)51,078(

)56,896(

)1( ���� ����� � ������� ����31 ����2013. )2( ������� �� ����� ������� ���� � ,�"�� ���� �� ������� ����� � � �� ���� �� ������

�� .����� � �� ����.����� �"�� ���� ��� ��� ����� �� ����� ����� ����� ���� �������� ������ ���� � ����� � � �� ����"�� ���� ��.

)3(� ���� ������: (�) ����� ���� ���� �� �������� ��� -N.V. NSI ���� ���- NSI �� �� ����50% .����� ���� �� , ��� � ������ ������ ���������20.54% �����N.V. NSI

������ � � �� �Habas Tulip B.V � ���� ������ �� ����Habas Star B.V. (�) . ������ ��� ����� ��� ������ ��� ����� ����� ��� ������1 . �������� �� ����� ������ ���� (�) :

11

���� ����� � �� ���� �"�� ���� ���� ������� ����� ��� (�) .������ ���� �� ��������� ��� - NSI N.V. �� �� ���� ���� ��� ,100% �� , ��� � ������ ������ ���������

.����� ���� )4(� ��������� � � ��� ����� ��� (�) : ������ �������� ����� ������ ���� �������- ��

���� (�� �� ���) ������� ��� ���� ��� ������� ���� � ��� ������� ���� ��������Dietikon �� �� �� �� � � �� ����� ���� ��� ������� ���� � ��� ������� ���� �������� �� ;�����

) ������1997) �"�� (�� :��" �� ������,(" � ����� ������� �� ����100% �� .����� � � �� � � �� ����� ����� ��������Habas Swiss Investments A.G. � ���� ������ �� ����Habas

Star B.V. (�) .� ������ ����) ������ ����� ������ ������ �����Mainstreet � � �� �������� (HRGI I B.V. �- HRGI II B.V. � ���� ������ �����Habas Star B.V. �� ���� ��� ���� (�) .

���� ���������� ����� ���� �����N.V. NSI ���� ����� ���� ��)����� ��- 6 (���� .����� � : (�) ���� ���� �� ���� ��� ����� ������ ���� ���� �����NSI N.V. ��)

���� ����� ���� �����- 7 (����(�) . � ������ ���� ���� ����� ������ ������ �����) ������Mainstreet(.

���� ����� ����NSI N.V. � ������ �����- Euronext ����� �� ������ ���� ,� ������.����� � ����� �������

)5( ,����� ����� ��� ���� ����� �� ���� ������ ����� ����� � ������ �� � ���� � ��� ������ ���� �� ,����� ���� ����� ������ ����� �� �� ����� ������������

��������� ������� ,����� .������ � ��� ������� �� ����� ����� ���� ����� ������ ����� �������� � ������ �������� ��� ���� ����� ����� ��� ,����� .������� ������ ����� �����

��� .��� �������� �������� ����� ��� ������� �� ��� ��� ���� ����� �� ����� ��� �� ����� �� ����1.1 ����� ����16 ���� � ������������ ��2012.

� �� ���� � ��� ���� ������� ����� ����-

-.��� ��� (���� ������) ����� ����� �� ������ ������ �������� - ������� ����� ����� ��� ���� ������� � ������� ���� ������ ���� ��� ������

.(������ ��� ;����) -.����� ������� �� ������ ���� ��� ������ - ����� ����� ��.����� ������� ������ ��� ����� ��

, ��� �� ���� � �� ������ ������ �������� ����� ,�� ������ ����� ,����� ������� ����� �"��� ,��� ����� ���� ��� ���- 1968 .� �� ������� ,��� ���� ������ �� ,������ ����� ����

������ ������� �� � ��� � � �� ����� ,������� �� ����������� ����������� ���� ,������� ������� ������ � � ����� �������������� ������ ��� ����� , ���� � ����� �� ������������� ������� ����� ,�� ��� . ������� ������ ,������ �� ����) ����� ������ �� �����

��� � ��� ��� ������ ��� ����� ������ �� ����� ����� �� ������� ����� ������ ���� (�� �� ����� ,����� �� ���� �� ����� ��� ����� � �� �� ����� ��� .�� ���� ����� ������ �� ����� ,�� ��� .����� � � �� ��� ��� ����� ����� �� ����� ����� �� ,��� �����

����� ���� ����� ��� ,�� ����� ����� ����� ����� �� ����� � �� ���� ����� ������� ������ ������ ����� ��� ������ ���� �� ��/� ������ ������ ,���� ��� ,������ �� ������ �� �����

.��� ��� ����� ���� � � �� ����� ��� ,���� � ��� ���

���� ��� ,��������� � �"�� ����� ��� �"�� ,

27 ���� 3201 ������ �����

��������������������� ������� ��������

) ������ �1960�"� (

����������� ���� �����������

� ���31 ���2013

(������ ���)

) ����� ���1960 (����� ������

����� ���� ����� ������ ����31 ���2013 (������ ���)

�������� ���

����� ���� � ����� �� 2

����� ������ ��������� ���� ������31 ���2013 (������ ���):

���� ����� ����� ���� �� ���� ����� 3

������� �� ���� ����� ����� ����� �� 4

������� �� ���� ������ �� ���� ����� 5

������� ��������� ������ �� ���� ����� 7

� ������� ����� ���� ������� �� ���� ����� 9

������ ��� ����� 8000 684 03 ������ �� KPMG �������� 8444 684 03 ������ ����17 ���� �� ,609 ����� www.kpmg.co.il

���� ��61006

���� ����� ������� ������ ,������ ���KPMG ��

� ��� ��� ������ �����- KPMG International Cooperative ,(“KPMG International”) .�������� ����

2

) ������ � �� ������ ���� ������ ��� ���� �� ����� ��1960� ("� ����

���� �� � ��� ����� ������ ) ����� ��� �1960�� (" ����) �� ��� ������ �- �� ����� ,(������ ���� ����� ����� ����� ���� �� �� � �����31 ����2013 �� ����� ����� ��������� ���� � ��� ��

������� ���� ����� ,����� ����� ������� � ������ ��� �� �� ������� ����� �����. ��������� ������� ������ ������ ������ � � �� ����� �� ����� ������ ���� ������� ������ ����IAS 34

������� ���� ���� " ����� ���� � ' ��� ��� �� ����� ������ ���� � �� ������ ������ �� ��� ,"������"�� ,(��� ���� �������� ���� ) ���-1970. ������� ��� ����� ���� �� � �� ���� ������ ����� ��

�� ������ ������. � ��� �� ���� �� ����� ����� � ����� ������ ������� � ������ ����� ������� ����� �� � ���-

8% ���� �� ����� ����� ����31 ����2013 ���� ����� ���� ����� ����� ������� ��������� ,����� � ��� �� ���� �� ,�� ��� .����� ����� ������� �� �� ��� � ������ �� ����� ������

������� � ������ ������� ��� ��� ����� �� ����� ���� ��� ��� �������� ������� �����- 28,946 ���� �" ����31 ����2013 � ��� �������� ������ � �����- 706 ��� � ������ �" ����

����� ����� ������� �� ��. � ��� ����� ������������� ������ � ���� ����� � � �� ��� ���� ���� ����� ���� ������ ��� ������ �� ��� ,������ ��� ������� ������� ���� ���� ����

,����� ������ ���� �� ������ � ���� ����� ������. ���� ������ ���� �� ������ ����� ���� ����� 1 � ��� ���� ����� ���� �����" � � �� ���� ������� �����

����� �� � � ����� ���� ����� � ."����� ����� � � �� ���� ������� ������ ����� ,�������� ����� �� ��� ������� ������ ,��������� ������� ������ ��� ����� ������� ������. ����� ���

������� ������ � ��� ���� ��� ������ ����� ����� ��������� � ������� ����� ������ ��� ����� �� ���� � ��� ������ ��� ������ ��������� ��� ������ ����� ������� ������. ����� ,���

��� �� ������ ���� �� � ������. ����

������ �� ������ ��� ���� ������ � ���� ���� ,����� �� ����� �� ���� �� ����� �� ����� � ��� ����� �"� ,���� ��� ��� ,�������� ������ ������� ������ ���� �����IAS 34.

����� �� �� ,����� ���� ���� � ������ ���� ��� ������ �� ������ ,�� ��� ������ ����� ������� ��� �"� ����� � ��� ����� �� ����� �� ���� ' ��� ��� ������ ������ ��� ,�������� ������ ��� ,��"�� ,(��� ���� �������� ���� ) ��� ����� ���� �- 1970.

�� ����� ��������� :����� ��� ���� �� ���� �� ,�"�

.� ����� �����1 � ����� ������ ���� ������ � ������ �� � �������� ����� �� � ����� ����� ��� �� ���� ����� � ������� ���� ����� �� � ����� ������12 �- 4 ��� �� ��� �������

�������2013 �������� ����� ������� ,�"� ����� �������� ����� ������ �� �� ,��� ������ .�� �� ���� �� ������� ���� � ."�� ���"� ����� � ����� ��� �� � ����� ���� ���� ,����

."�� ���"� ������ ����� ���� �� ����� �� ���� ������ ���� ,������� ����� � ������������

.� ����� �����5 ����� ������ ���� ������ ����� ������ ���� �� �NSI ��� ������� ������ ���� ,� ����� � ���� ����� ,����� ���� ��� ���NSI .������ �� �������� ������� �� � ������ ������

.� �������� �����7� �-7 ������ ����� ����� � ���� ������ �� � ����� ������ ���� ������ �

.�������� �������

�� ����,

������ ���� ���� ����

27 ����2013

) ����� ���1960 (����� ������

���� ���� ����� ����� ��� �� ���� �����

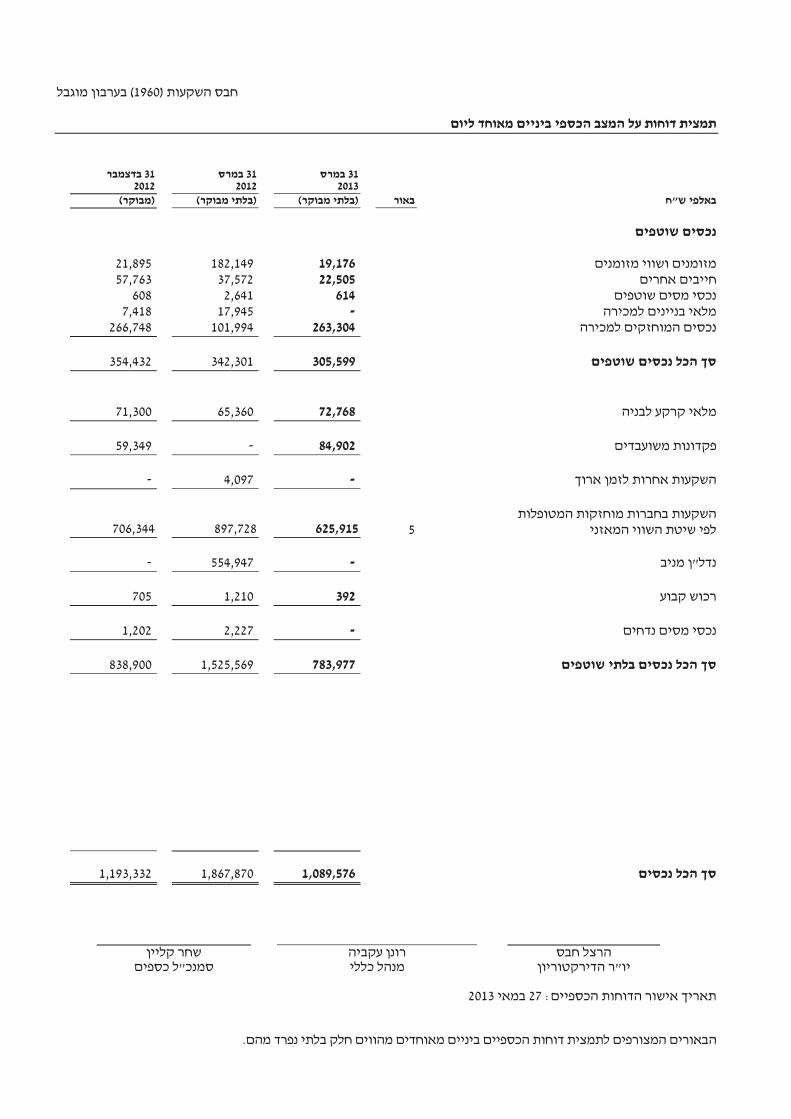

31��� 31��� 31 ���� 2013 2012 2012

"� ���� ��� (���� ���) (���� ���) (����)

������ �����

������ ���� ������ 19,176 182,149 21,895

����������� 22,505 37,572 57,763 ����� ���� ��� 614 2,641 608

������ ����� ���� - 17,945 7,418 ������ �������� ���� 263,304 101,994 266,748

������ ����� ��� �� 305,599 342,301 354,432

���� ���� ���� 72,768 65,360 71,300

��� ���� ��� � 84,902 - 59,349

���� ���� ����� ����� - 4,097 -

������� ������ �������������

����� ���� ��� ��� 5 625,915 897,728 706,344

��� �"� - 554,947 -

���� ��� 392 1,210 705

������ ���� - 2,227 1,202

������ ��� ����� ��� �� 783,977 1,525,569 838,900

����� ��� �� 1,089,576 1,867,870 1,193,332

���� ��� ����� ��� ����� ��

��������� � �"�� ���� ��� �"��� �����

:������� ���� � ���� �����27 ����2013 �.��� �� ���� ��� ������ �� ���� ����� ������� ���� ������ �������� ������

3

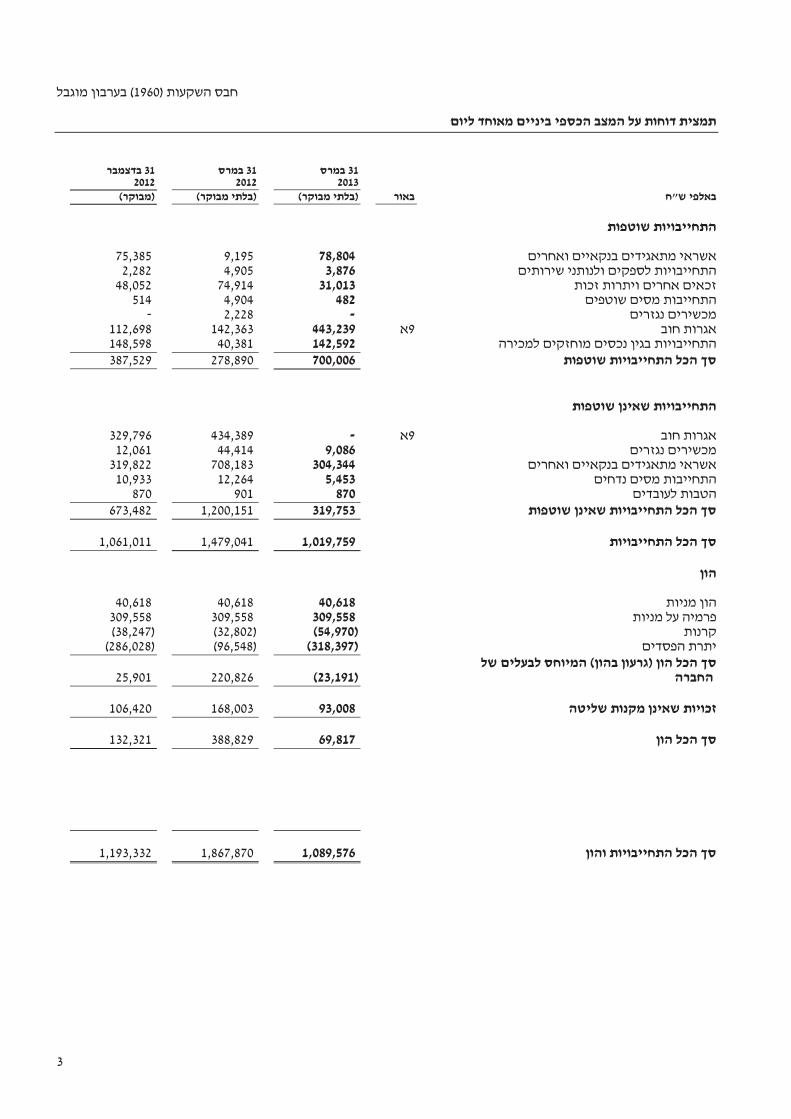

) ����� ���1960 (����� ������

���� ���� ����� ����� ��� �� ���� �����

31��� 31��� 31 ���� 2013 2012 2012

"� ���� ��� (���� ���) (���� ���) (����)

������ ��������

������ �� ����� ���������� 78,804 9,195 75,385

������ ����� ������ ���������� 3,876 4,905 2,282 ����� ��������� ������ 31,013 74,914 48,052

������������� ���� 482 4,904 514 ����� ������ - 2,228 -

��� ����� 9� 443,239 142,363 112,698 ����������������� ���� ���� ������ 142,592 40,381 148,598

������ �������� ��� �� 700,006 278,890 387,529

���������� ��������

��� ����� 9� - 434,389 329,796 ����� ������ 9,086 44,414 12,061

����������� �� ���� ������ 304,344 708,183 319,822 ����������� ���� 5,453 12,264 10,933

�� ���� ����� 870 901 870 �� ���� �������� ��� ������ 319,753 1,200,151 673,482

�������� ��� �� 1,019,759 1,479,041 1,061,011

��

���� ��� 40,618 40,618 40,618

���� �� ����� 309,558 309,558 309,558 ���� )54,970( )32,802( )38,247( ������ ��� )318,397( )96,548( )286,028(

�� ��� �� ( �� ����) �� ����� ����� ��� )23,191( 220,826 25,901

����� ����� ���� ������ 93,008 168,003 106,420

��� �� �� 69,817 388,829 132,321

�� �������� ��� �� � 1,089,576 1,867,870 1,193,332

4

) ����� ���1960 (����� ������

��������� ����� ���� �� ���� �����

��� �������� ����� ����� �� ������ ��� �������� ����

31��� 31��� 31 ���� 2013 2012 2012

"� ����(���� ���) (���� ���) (����)

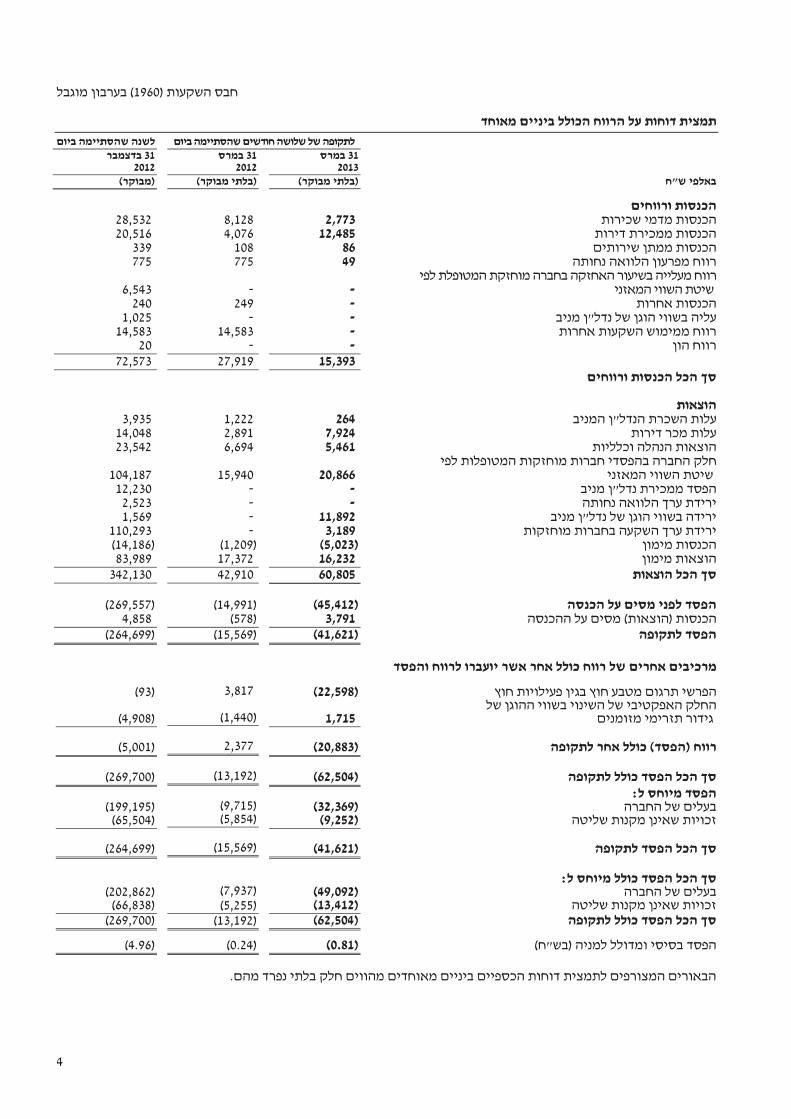

������ ������ ����� �� � ����� 2,773 8,128 28,532

���� ������ ����� 12,485 4,076 20,516 ������ ���� ����� 86 108 339

���� ������ ������ ���� 49 775 775 ����� ������ ����� ��������� ������� ������ ����

�������� ���� - - 6,543 ����� ����� - 249 240

��� �"� � ���� ���� ���� - - 1,025 ����� ����� ����� ���� - 14,583 14,583

��� ���� - - 20 15,393 27,919 72,573

������ ������ ��� ��

������ �� �������� �"� � �� 264 1,222 3,935

���� ��� ���� 7,924 2,891 14,048 ������� ���� ������ 5,461 6,694 23,542

��� �������� ������� ����� � ���� ����� ��� ����� ���� ��� 20,866 15,940 104,187

��� �"� ������ ��� - - 12,230 ���� ������ ��� � ��� - - 2,523

��� �"� � ���� ���� � ��� 11,892 - 1,569 ������� ������ ���� ��� � ��� 3,189 - 110,293

����� ����� )5,023( )1,209( )14,186( ����� ������ 16,232 17,372 83,989

������ ��� �� 60,805 42,910 342,130

����� �� ���� ���� ���� )45,412( )14,991( )269,557( ) �����������( ����� �� ���� 3,791 )578( 4,858

������ ���� )41,621( )15,569( )264,699(

�� ���� ��� �� ���� ����������� ���� ����� ���

� ������� �������� ���� ��� ���� ���� )22,598( 3,817 )93( � ����� ���� ���� � �������� ����

������ ������ �� �� 1,715 )1,440( )4,908(

��� (����) ������ �� ���� )20,883( 2,377 )5,001(

������ ���� ���� ��� �� )62,504( )13,192( )269,700( :� ���� ����

����� � ����� )32,369( )9,715( )199,195( ���� ���� ��� ������ )9,252( )5,854( )65,504(

���� ��� �� ������ )41,621( )15,569( )264,699(

�� ��� ���� :� ���� ����

����� � ����� )49,092( )7,937( )202,862( ���� ���� ��� ������ )13,412( )5,255( )66,838(

������ ���� ���� ��� �� )62,504( )13,192( )269,700(

(�"�) ���� ��� �� ����� ��� )0.81( )0.24( )4.96(

�� ���� ��� ������ �� ���� ����� ������� ���� ������ �������� �������.���

5

) ����� ���1960 (����� ������

������� �� �� �������� ������ �����

���� ������

��� �� ����� ���� ����� ����� �� ��� ��

�� �� �� ��

����� �� ����� ��

�� ����� ������ �� ���� �� �� ���� ���� "� ����� �� ����� �� ����� ����� �� ������ ��� ��

�� ����������� �����

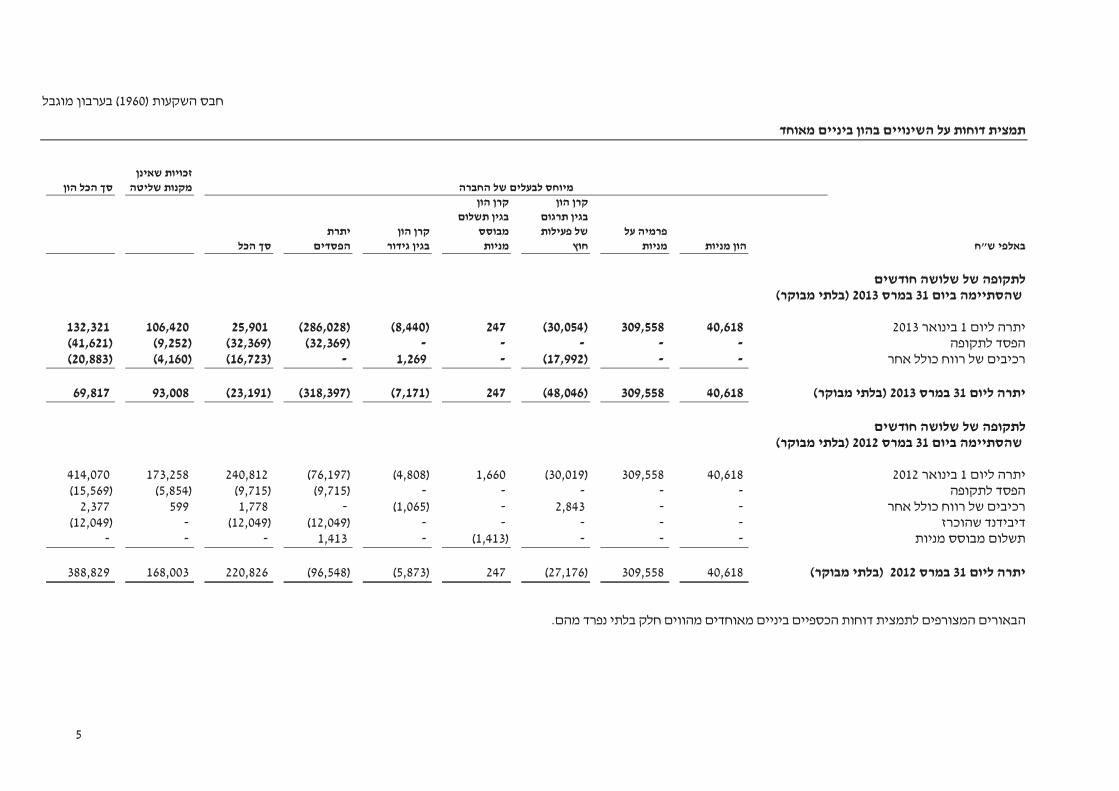

���������� �31���2013(���� ���)

���� ����1�����2013 40,618 309,558 )30,054( 247 )8,440( )286,028( 25,901 106,420 132,321 ������ ��� - - - - - )32,369( )32,369( )9,252( )41,621(

��� ���� ���� � ������ - - )17,992( - 1,269 - )16,723( )4,160( )20,883(

���� ����31 ���2013 (���� ���) 40,618 309,558 )48,046( 247 )7,171( )318,397( )23,191( 93,008 69,817

�� ����������� ����� ���������� �31���2012(���� ���)

���� ����1�����2012 40,618 309,558 )30,019( 1,660 )4,808( )76,197( 240,812 173,258 414,070

������ ��� - - - - - )9,715( )9,715( )5,854( )15,569( ��� ���� ���� � ������ - - 2,843 - )1,065( - 1,778 599 2,377

����� ��� - - - - - )12,049( )12,049( - )12,049( ���� ����� ���� - - - )1,413( - 1,413 - - -

���� ����31 ���2012 (���� ���) 40,618 309,558 )27,176( 247 )5,873( )96,548( 220,826 168,003 388,829

�.��� �� ���� ��� ������ �� ���� ����� ������� ���� ������ �������� ������

6

) ����� ���1960����� ������ (

(����) ���� ����� �� �������� �� ���� �����

���� ������ ��� �� ��� �� ����� ���� ����� ����� �� �� �� �� �� ����� ������� �� �� ����� ����� ��������� ����

"� ���� ����� ��������� ����� ����� �� ������ ��� ��

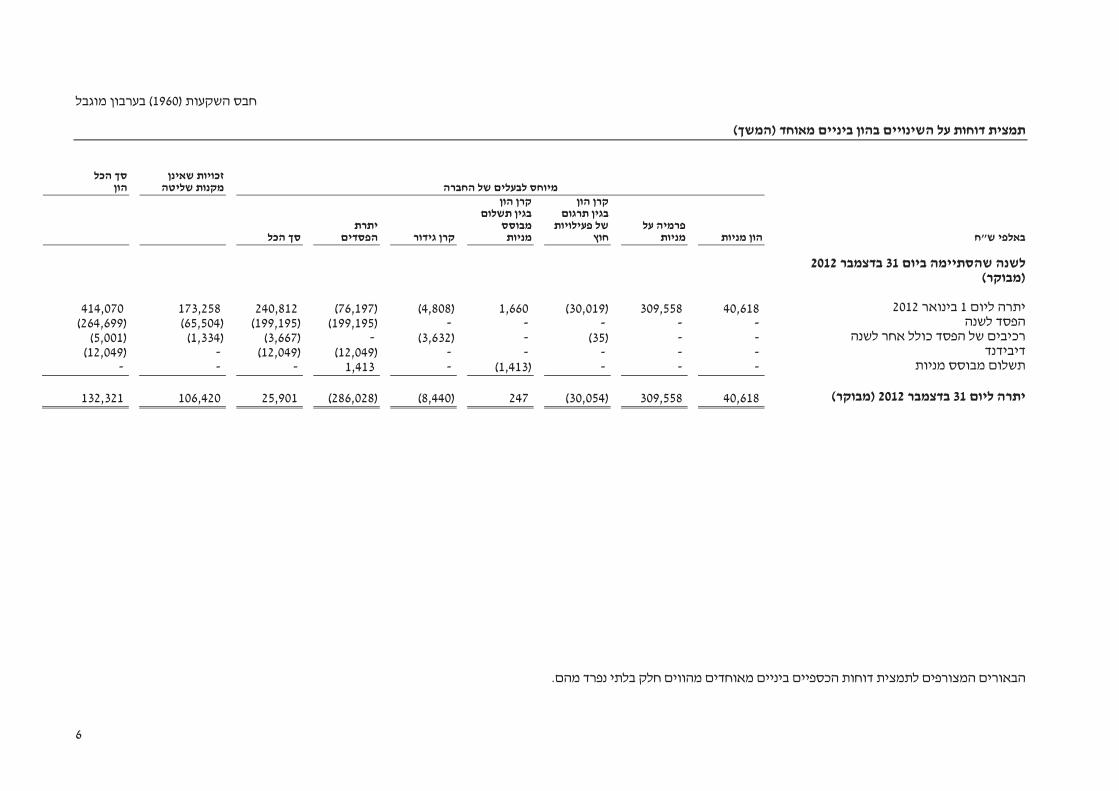

��� �������� ����31����2012 (����)

���� ����1�����2012 40,618 309,558 )30,019( 1,660 )4,808( )76,197( 240,812 173,258 414,070

��� �� - -- -- )199,195( )199,195( )65,504()264,699( ��� � ��������� ������ - -)35( -)3,632( -)3,667( )1,334()5,001(

��� - -- -- )12,049()12,049( -)12,049( ���� ����� ���� - - - )1,413( - 1,413 - - -

���� ����31����2012(����) 40,618 309,558 )30,054( 247)8,440( )286,028( 25,901 106,420 132,321

������� ��������� ����� ������� ���� �� ���� �����.��� �� ���� ��� ������

7

) ����� ���1960 (����� ������

������� ���������� ������ �� ���� �����

��� �������� ����� ����� �� ������ ��� �������� ���� 31��� 31��� 31 ����

2013 2012 2012 "� ���� (���� ���) (���� ���) (����)

������� ������������ ������

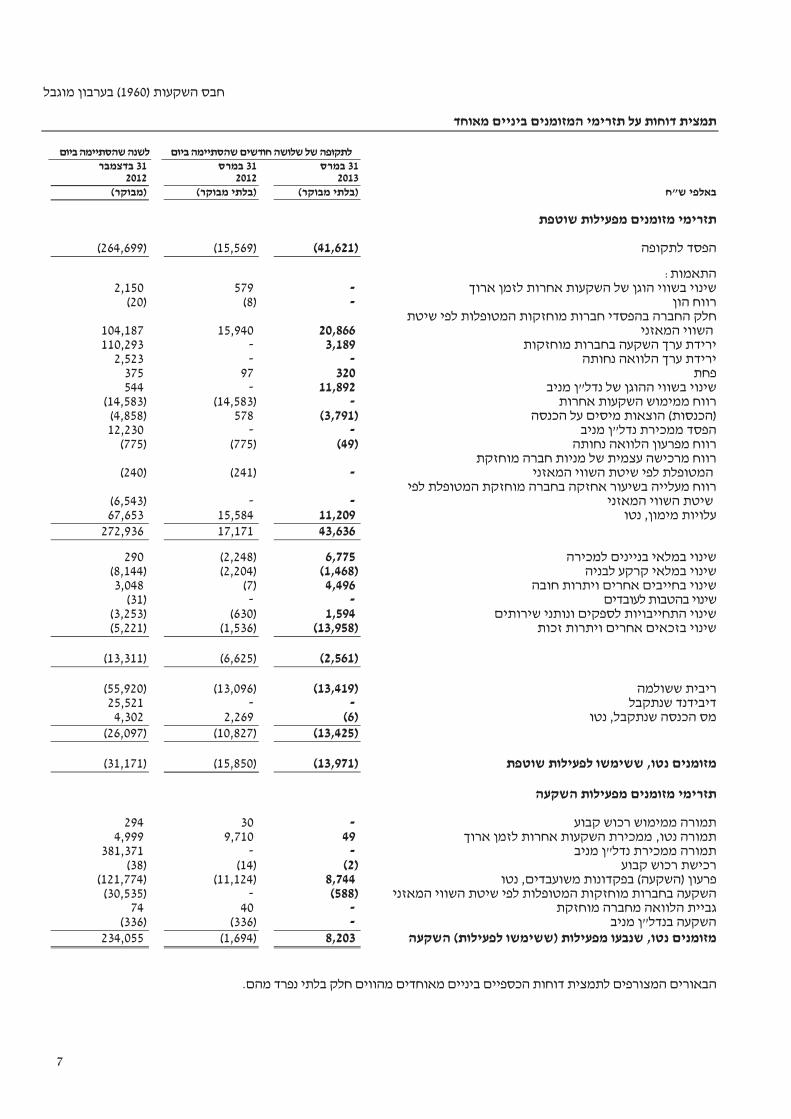

������ ��� )41,621( )15,569( )264,699(

������: ���� ���� ����� ����� � ���� ���� ��� - 579 2,150

���� ��� - )8( )20( � ���� ����� �������� ��� �������� ����������

����� ���� 20,866 15,940 104,187 ������� ������ ���� ��� � ��� 3,189 - 110,293

���� ������ ��� � ��� - - 2,523 ��� 320 97 375

��� �"� � ����� ���� ��� 11,892 - 544 ����� ����� ����� ���� - )14,583( )14,583(

(�����)���� �� ����� ������ )3,791( 578 )4,858( ��� �"� ������ ��� - - 12,230

���� ������ ������ ���� )49( )775( )775( ������ ���� ���� � ����� ����� ����

������������ ���� ��� ��� - )241( )240( ��� ������� ������ ����� ����� ����� ������ ����

����� ���� ��� - - )6,543( �� ,����� ������ 11,209 15,584 67,653

43,636 17,171 272,936

������ ����� ����� ��� 6,775 )2,248( 290 � ������� ���� ���� )1,468( )2,204( )8,144(

��� ����������� ������ ����� 4,496 )7( 3,048 �� ���� ������ ��� - - )31(

� ���������� �������� ������ ���� 1,594 )630( )3,253( ���� ������ ����� ������ ��� )13,958( )1,536( )5,221(

)2,561( )6,625( )13,311(

���� ����� )13,419( )13,096( )55,920(

���� ��� - - 25,521 �� ,���� ���� �� )6( 2,269 4,302

)13,425( )10,827( )26,097(

���� ����������� ������� ������ , )13,971( )15,850( )31,171(

������� ������������ ������

���� ��� ����� ����� - 30 294 ,�� ����� ���� ���� ����� ����� ������ 49 9,710 4,999

��� �"� ������ ����� - - 381,371 ���� ��� ���� )2( )14( )38(

�� ,�� ���� ��� ��� (����) ����� 8,744 )11,124( )121,774( ����� ���� ��� ��� �������� ������� ������ ���� )588( - )30,535(

������ ����� ������ ����� - 40 74 ��� �"� � ���� - )336( )336(

�� ��������, (������� ������) ������� ��������� 8,203 )1,694( 234,055

� ��������� ������ ����� ������� ���� �� ���� �����.��� �� ���� ��� ������

8

) ����� ���1960 (����� ������

������� ���������� ������ �� (����) ���� ����� ��� �������� ����� ����� �� ������ ��� �������� ���� 31��� 31��� 31 ����

2013 2012 2012 "� ���� (���� ���) (���� ���) (����)

������� ������� ���� ������

��� ����� ����� ����� - 54,922 54,922

��� ����� ����� - - )146,574( ���� �� ��� - - )12,049(

����� ������ ����� ���� ���������� 4,266 - 11,731 ����� ������� ����� ���� ���������� )5,022( )1,027( )291,936(

����� ��� ���� ���� �������� , 3,632 )764( 54,249

,��� ������� ���� (������� ������) ������� ���� 2,876 53,131 )329,657(

( ����) ����� ,���������� ����� ������� )2,892( 35,587 )126,773(

������� ������ ������ ���� ����� 21,895 147,161 147,161

������ ����� �� ������� ��� �� �� ���� ���� ������ 173 )599( 1,507

������ ���� ������� ����� ������� 19,176 182,149 21,895

�.��� �� ���� ��� ������ �� ���� ����� ������� ���� ������ �������� ������

) ����� ���1960����� ������ (

(������ ���) ������ ����� ������� ����� ������ �����

9

���1 - ����

.� ������ �����

) ����� ���1960 �"��� ���� ��� ����� ������� ����� � ���� �� ���� ��� ("�����" :����) �"�� (18 ��- ���� ������ � �� ����� ������� ���� � ����� .����31 ����2013 �� ����� � ��� �� ������ ,

.������ ������ ������ ������ �� ��� ,("������" : �� ����) �� ���� ������ ,����� ����� ������ ��� � ����� ���� ,������ ,����� ����� ������ �� ��� ���� ���� ,����

����� ����� ����� � ���� ����� .�"� �� ��� �������� ������ �"� � ����� �������� � ������.���� ��� ��� ������ ������

. "� ���"� ��� �� ����� ���� �� ��������� �����

����12 ����2013 �� ����� ����� ("���� � ���" :����)� ��� ���� ����� ���� �� �� �� ���� ��� � � ���

������� ��� ���2013 ,�� ����� N.V. NSI� � ����� ������� ���� ���� ����� ���� ,- 20.54% ��" :����) ������ � �NSI(" ��� �� ������� ������� ������� ����� �������� ����� ����� ���� ,

���� � ��� ,���� ���� ���� ��� ��� ���� .�� ������ ������ ������ ���� � ���� � ���� ���� ����� � ������� ������ �� ���� �� ����� �� ������� ����NSI ��� �� ���� ,������� � ��� ��� ,

� ������ ���� � ����NSI ��� ����� ����� ���� ����� ���� ��� ������ ������ ����� ���� ���� .��� �����

�� � �������� ����� ����� ,������� ������ ������ ������ ���� � �� ���� ����� ,��� �� ��� �� ��� �� ���� ����� � ������� ���� ����� �� � ����� ������ ����� ����� � ������12 �- 4 �������

�� ��� �� ��� �����2013 ���� ����� �� �� �� �� ���� ������ ����� ����� ��� ,����� ����� ..��������� ����� ���� ����� ������ ��� ����� �� ����� ����� ������

���� ����� ���� ,����� ��� �13 ���� 2013 ��� �� ���� ����� ������ ����� �������� ��� ��12 �- 4 ,

� ����� ���� �� ,�� ����� ������ ����� ������� ������ ������ ���� �� ,���� ��� ,����� ������� ������������ ��� ����� ��� ��� ������� ��� ������ ��, �� �� �� ����� �� ������ ��� �� ��� ��

����� ��� ������ ����� ����� ,����� ������� ���� ������ ���, ����� ��� ���� ��� ���� ����� ����� ������ �� ��������� ��� ������ ����� ������� �� ��� .�� �� ������� ���� ����� �������

) ������ ����� ��� ���� ���� �� ����Margin Call ���� ���) (17� ����� ���� � �� ��� ���� ���� ,(��� ������� ����� ��4 ����� ���� ��������� ��� .���� ������ ����� �� ���� ����� ��� ����� ���

.� ;������ ����� �� ����� ����� ��� �� �� ���� .� :���� � ���� �� ������ ���� ��� ����� ����� ���14 � ;������ ����� �� ������ �� ����� ����� �� �� �� ����� ����� ��� ���� ����� ��� � �� ���� .

.���� ��� � � �� ���� ����� ������

��� �� ���� ����� ������ �����12 �- 4 ���� ������� ,18 ����2013 ����� ��� �� ��� ��� ����� ���� , ���� ���� ��� �������� ��� ����� ��� ���� �� ����� �� � ����� ����� �� ,���� ����� �����

.("������" :����) ������ ������ � �������� ������ �� ������ ������ �� ����� ����� ����� ������� �� � ����� ����� �������� �������� ����� �� ,����� � ���� �� ��� ��������� ,����� ���� ��� �� � ����� �� �

���� �� � ���� ����� ������ ��� �� ����� .����� ���� ����� ������ ����� �� �� ����� �����6 ,7 �-9.

����13 ����2013 �� �) ���� ������ ���� �� �� �� ����� �����12 ��� � ���� ���� �� � ����� � ( �� �) ��� ����� � ������ ��� �����12�� ������ ����� ��� �� ��� ,( ��31 ����2013 ���� ,17 ����2013.

���� 19 ����2013 , ����������� � � �� ��� ����� ������ ����� ���� ���� ������ ,����� ,����� ����

���� ������� ������ �������� ����� ���� ����������� �������� �� �18 ����2013, ����� ����� ������ ���� �� ��� ���� ������� ������� �� ����� ���� ����� ������ ������ �� ��� �, ����

���� ��� ���� ����� ��� � ��� ����� (��� �� ��) ���� ����� ��� � � ������ ������ ���� �� � ����� �� �) ��� ����� ������12�� , ��� ����� � (������� � �� ��� ���� � ���� � ���� �� � � �������

12 ���� �� ������ ������ �) ��� �� 26 �����2013.( ��� �� � �� �� ����� ���� ���� ��� �� ������� ��� .

���� ������ ������� ."�� ���"� ����� � ����� ��� �� � �������� ����� �������

���� ����� �� ���� ������ ����� ���� ��� ,����� ���7.

���� �� ����� �� ,���� ������ ���� ������������ ����� ���� ���� ������ �� ���� �� ������� ���� �

."�� ���"� ������ �����

) ����� ���1960����� ������ (

(������ ���) ������ ����� ������� ����� ������ �����

10

���2 - ������� ����� ����� ���

.� ��������� ���� ���� ���� ����� �� �����

����� ���� � ������ ����� ���� �� ����� ������ ��- 34 IAS����� ������� ���� ���� , ���� ���� ������� ���� � �� ��� ���� ����� � .����� ���� ������ ���� � � � � ��� �� �� �����

���� ������� ���31 ���� �2012 �� ���� ��� ���� ,�� ��� .("����� ���� �" :����) ��� �"�� ,(��� ���� �������� ���� ) ��� ����� ����� ' ��� �������- 1970.

���� ����� ��������� � � �� ������ ���� �� ����� ������ ������� ���� � �����27 ����2013.

. ��� ������ ������� �����

� ����� ������ ���� � ������ �� ����� ������ ������- IFRS �� ,������� ����� �

���� � ������� ��� ���� �� ���� �� ������ �� ����� �� ��� ,������� �� ����� .������� ����� ,����������� �� ���� ��� ����� ������ ����� ������� ��������.

� ������� ���� �� ���� ��� ,����� � �� � ���� ������� ��� �������� ������ ������

.����� ������� ���� � ��� ��� �� ������ ��� ,��� �� ��� �������

���3 - ������� �������� �����

��� ,��� �� ���� ����� ������ ���� ������ ������ � ������� ���� �� ,���� ������� ������ ���� ���� ��.����� ���� � ����

:������ ��� �� ���� ����� ������ ���� ������ ������� ���� �� ��� ������ ���� ����� ����

���� ����� �� ������� �����

���� ���1 �����2013 :���� �������� �������� �� �� ����� �� ������ ����� )1( � ����- 1 IAS, ��������� ���� �

����� ���� ��� ���� ���� ����� �� ,������� ���� � ��� ���� ���� ����� � ����� ���� �� �� ������ ����� ������ �� ����� ��� ���� ���� ������ ��� ����� , ���� ����� ������ ����� ����� ������ �����

. ����

���� ����� �� ������ ����� .������� ���� � �� ������ )2( ���� ������ ������ �� �������� ������� ������ ,������ ���� ���� ���� ����� �� ��� �����

������� ���� ���� ��IFRS 10 ,������ ������ ����

� ������ ��� ���� ,������ ��� � ��� ������ � ���� � �� ���� ���� ����� ,���� ����� .������� .���� ���� ����� ������� �������� ���� � ����� �� ,���� ����� ����� ����� ����� "���� � " ������ �� ��� ,�������� �� ����������� ������ ������ �� ����� ����� ,���� � ����� ������ ,����

��� ����� ���������� �����.� ��� ��

.������� ���� � �� ������ ���� ����� �� ���� �����

.(����� ������� ������� ����� ����) ����� ��� ����

������� ���� ���� ��IFRS 13 ��� ���� �����

�� � ����� ����� ����� � ����� �� ����� ����� � �������� � ����� ���� � � � ���.�� �"� � �� ������ �� ���� ��� ��� ����� ������� ������ ��� ����� �"� � ���� ��� � � � ������ � � �� ����� ����� ����� ����� �� ������ �� ,��� ������� ���� ��� ���� �������� �������

.� � �� ���� ���

) ����� ���1960����� ������ (

(������ ���) ������ ����� ������� ����� ������ �����

11

���3 - ������� �������� ����� �)(���

���� ����� �� ������� ����� (����) )2( ���� ������ ������ �� �������� ������� ������ ,������ ���� ���� ���� ����� �� ��� �����

(����)

������� ���� ���� ��IFRS 13 ��� ���� ����� )����(

� ���� � ���� ���� �� � ��������� �� ��� ��) ���� ���bid price���� ����� ����� ( )ask price ,(.���� ��� � �� � � �� ������ ���� ��� ����� ���� ����� ����� ����� ����� ���� �����

��� ��� ������� ������ � �� �� ����� �� ���� � ������ ���� ��� ���������� ����� ���� ���������� �����.�

�� ���� ���������� ������� ���� � �� ������ ����.

���4 - ����� ����

����� ���� ��� ��� ������ ������ ����23 .���� ����� ���� ,����� ���� � ������ ����� �� �

� ��� �2012:���� � ��� ��� ������ ��� ��� ������ ,

��� �"� - ,����.������ ����� ����� ����� ������ �� ��� ���� ��� � ����� ���� ������ �"� - .����� ������ �"� � ����� �������� � ������ ���� ,���� ,�����

�"� ��� �����- .������ ����� �"� �� ��� ������

�� ���2013 ������ ������ ��� ���� ��� ����� ����� ��� �� ������ ������ ,����� .�"� � ������ ��� ���.���� �� ����� �� ������

���� ��� ������� ������ �� ����� ������ ����� ���� �� ���� ��� ���� �� ������ � ������ �����

.������� ������

� ��� ��� ������� ������� � ������� ���� �� ����� �����3 .����� ���� �

.�� ���� ������ ���� ����� ����� ,������ ������ ,������� ��������� ������ ������

.� ���� �� ������ ����� ����

"� ���� ��� "��������� "��������� �"��

����� ����� �� ������ ��� ��������31 ���2013

(���� ���)

�������� ������� ����� �� 2,773 12,485 135 15,393

������� ( ���) ���� )9,383( 4,561 )5,326( )10,148(

����� � �� ,�� ���� ��� ��� ��� �������� �������

����� ���� )20,866( - - )20,866( ������ ����� ���� ��� � ��� )3,189( - - )3,189(

����� ( ���) ���� �� )33,438( 4,561 )5,326( )34,203(

) ����� ���1960����� ������ (

(������ ���) ������ ����� ������� ����� ������ �����

12

���4 - (����) ����� ����

.� (����) ���� �� ������ ����� ���� "� ���� � ������

��� "��������� "���"��� ������ �"��

����� ����� �� ������ ��� ��������31 ���2012

(���� ���)

�������� ������� ����� �� 8,368 4,085 775 108 13,336

������� ( ���) ����6,319 1,244 688 )5,722( 2,529

� �� ,�� ���� �������� ��� ��� �������� �������

����� ���� )15,940( - - - )15,940(

����� ( ���) ���� �� )9,621( 1,244 688 )5,722( )13,411(

"� ���� � ������ ��� "��������� "��� "��� ������ �"��

��� �������� ����

31 ����2012 (����)

�������� ������� ����� �� 36,340 20,516 775 359 57,990

������� ( ���) ����13,805 6,468 )2,815( )17,315( 143

����� � �� ,�� ���� ���

��� ��� �������� ������� ����� ���� )104,187( - - - )104,187(

������ ����� ���� ��� � ��� )110,293( - - - )110,293(

����� ( ���) ���� �� )200,675( 6,468 )2,815( )17,315( )214,337(

����� ��� �� ���� �� ������ � ������

��� �������� ����� ����� �� ������ ������ ������ 31 ��� 31 ��� ���31 ���� 20132012 2012

"� ���� (���� ���) (���� ���) (����)

���� ��� ������ ���� ������� ���� ��)34,203( )13,411( )214,337( ����� �� ���� - 14,583 14,583

�� ,����� ������ )8,169( )16,163( )69,803(

���� �� ���� ��� ���� ��� )42,372( )14,991( )269,557(

) ����� ���1960����� ������ (

(������ ���) ������ ����� ������� ����� ������ �����

13

���5 - ������ ����� ���� ��� �������� ������ ���

� ������ ������� ���� � ����� �� ��� �� ���� ����� ������ ���� ������ ����� ������NSI .

� ���� � ���� ����NSI .����� ��� , �� ��� ��� ���� ����� � ������� ��31 ����2013 ���4.6612.

:���� � ������ ����� � ������� ���� ��� ���� ����� ����

����� ��� ����� �� %

:���� ������� �� �� ��� � ������ 31 ����2013 )5.27( 31 ����2012 0.40

���� ������� ��31���� �2012)0.35(

����NSI � ������ �����- Euronext NYSE Amsterdam ("������" :����). � ����� ����- NSI ���� ����� � ���� ��� ����� ����� �� ��� ��� .����� ���� ��� ��� �����

� �����NSI��� � � ���� ����� . ����� ���� ����� � ��� .��� � ��� �� �� ���� ����� ���� �� .����� � ���� �� ���� �� ������ ���� ������� ��� ������ �������

����� ������ ����11 ���� ����� ���� � ��� ������ ,����� ���� � NSI �� � ����������� �����

����� ������ ���� ����� ��28 � ���� ����� ����� ��� � ���� ����NSI ����31 ����2013 , ���� ��� �� ,�� �� � ����� �� ,���� ������ ������ ����� ���� ���� ����� ��� ����� �������

�� ��� ��� � ���� ����� ���� ,��� � ����2012 ����� ����� � ���� �� ����� .NSI � ���31 ����2013 ���618,073 ,�" ���� ��� � ��� ��� ������ ����� ���� :�����- 722,551 ����� �" ����

� ��� � ���� ����104,478 �� � ��� ������ ����� ���� �� ,�" ����618,073 �� ������ �" ����� ������ � ����-NAV � (�� ��� ���)NSI ��� �- 132.6 .���� ������

������ ,�� � ������������� � ��� �� ���� �NSI�� ,B.V. Habas Tulip " :����)Habas Tulip(" ����

, ���� ����� � ����� � ���� ����� �� ������ ���� ���� �����- Habas Tulip ������ �� ����� ������NSI ����� ������)17� �� ������ �� ����� � �� ���� ,������� ������� �� ��� ,(

������ � ��� ��� � �����LtSV.

� � ��� ���� ������ ���� � ��� �� � ������ ,�� ������- 6.1 �) ���� ������- 30 ���� ��� �� (�" ������31 ����2013� ��� ����� �� ��� ���� ,- 18.2 ���� ������ �)- 85 � ���� ���� � ���� ��� .(�" ������-

LtSV ���51.40% ����� ���� �� ������ ������ � ��� ��� ���� � ��� �� ���� .)Waiver letter ( �����Habas Tulip ���� ,25 ����2013 ��� ������ ����� ���� ,������ ����� ��� ,25 ����2013 ��5 ������

2013 � ��� ("������ �����" :����)- LtSV �� ��Habas Tulip ����� �� ������� ����� ����� ���� �� ���� �� ,������55% ���)50% ��� ����� ����� ��� ������ ������ ����� (������� ����� �����

� ���� ������ ������ ��/� ���� �� ���� ����� ������ ���� ����� .������ ���� � ��� ���� � ��� ����� � ��� ����� �� ����- 18.7 �) ���� ������- 87 .(�" ������

:����� ���� ��� ��� ,���� ����� ����� �� ���� �� ��

�. � � ��� �������- 3.8 � ����� ���� ������ ���� ������- Habas Star �����11 �������2013 �- 14

����2013 ���� ��� �� ����� .6.�

�. ����� �������Habas Star ���) ������ �����-(��� ����21 ����2013�) ����� � ���� .- 0.9 ������ ���� ����� (���� ���� ����� ��� �� �����12 �- 4 ���� ����� ��� ��21 ����2013 ������ �� ,

� ��� �� ����� � ���� ����� ������ ����� ���� ������ � ������ ����� � ����� �� ����� ��� ����.

) ����� ���1960����� ������ (

(������ ���) ������ ����� ������� ����� ������ �����

14

���5 - ������ ����� ���� ��� �������� ������ ��� (����)

�. ����� �������Habas Star ���) ������ �����-(��� ����5 ������2013�) ����� � ���� .- 0.5 ������ ���� ����� (���� ���� ����� ��� �� �����12 �- 4 ���� ����� ��� ��5 ������2013 ������ �� ,

������ ����� � ����� �� ����� ��� � ��� �� ����� � ���� ����� ����� ���� ������ �����.

������ �� ��� ����� ���� �� ��� �� ������ ���������� ���� ����� ������21 ����2013 ���� ��� ,1.�

���� � ���� ,��� ������ ���� ����� ���� �����NSI ��� �� �� ����� ,������ � � �� ��������

��� ,����� � �������79 �) ���� ������- 377 .(�" ������

� ���� ,�� � ����� ���� ���- LtSV � ���- 45.8%.

���6 - � ���������� ����

.� ����4 ����2013 ��� ��� ����� ���� ���" :����) ����� � � �� ������ ������� ���� ,�"�� ("������� ���� � ��� ��� ��� '��� ��� � ���� ������ ����� ������ ������� ���� ���-

� ��� ���� ���� ������ ("���" :����) ����15 � �" ������ � ����� ��� ������ � � �����8.3% ���� �� ����� ������ ����� ������� ��� .������ ��� ���� ������ .������ ������ � ���

������ .��� ��� ���� �� ������� ����� ������ ������� �� ������ ����� .������� ������ ����� ���� ��� � ��� ,������� ������ ���� ����� .��� �������� �� ,���� ��� � ���� �����

��������������� ��� ������ ����.

.� ����� ������ ����5 �� � ������ , �����Habas Star � ����� � ����� ������� ��- Habas Star � ����� ����� �������)- Habas Star���� � ,("����" :����) (:

)1( � � ��� �����2.5 ,���� ������ ���� ������11 �������2013 ������� .�� ����� ��� �����

�12% � ��� ���� ������31 ����2013 ) ���� �� ������� ����� ��� ,���� ������30 ����2013� ����� ����� .(� ������ ���� ������� ����� ���� �� ����� ������� ,����� �� ��

����� �� ���� ��������� ����� ����� �� ���� ����� �� ���� �� ���� ���� ����� ����� ���� �� ������ ����� � ����- Habas Star �� ��� .��� ��� �� ����� ������

�������Habas Star ����� ���� �� ������ ����� �� �� ������Habas Star��� �� , ����� � ���� � ��� (������ ���) ������� ���� ���� ����� ��� ��� �� ���� ������

����� ,����� ����Habas Star � ��� ������ ����4 ����� ������� ����� .���� ������ ���������Habas Star ����� ������������ � ���� �����74% ��� ��� �� �� ��������

�� � �Habas Star ���� ���� ������� ������ ��� � ���� ��� �� �� ,7 ���� ����� ��� .������� ������

����1 ����2013 ����Habas Star � ��� ������� � ���� ������1 ��� ����� ��� ���� ������

���� � ������� ���� ������ ��� ���� �� �� ��31 ����2013 . ����13 ����2013 ����Habas Star � �� ��� ������� ���� ��- 1.57 �) ���� ������- 7.4 ��� � ���� ������ ���) (�" ������.(��

) ����� ���1960����� ������ (

(������ ���) ������ ����� ������� ����� ������ �����

15

���6 - ��� ����� ������� (����)

.� (���)

)2( ������ � ���1.3 ���� ������ ���� ������ ,14 ����2013 , � � ������90 ��� ���� ,��� ���� � ������13 ����2013 � ����� ��� ����� ��� ,("������� ������ ���" :����)12%

��� ���� ���� ������� ("������" :����)("����� ����" :����) ���� � ,�: ���� ��� �� ������� � ��� ����NSI ������Euronext � �� �� ,5.36 ���� ��� .����

���� � ������ �� �����NSI ����� �� ���� ��� ������� ����� ��� ���� ,���������� ���" :����) ����� �������NSI � ���� ���� ,("����� ������� ����- 5.36 ���� ,���� ����

�� ����� ����242,537 � ���� �� ��)1.3 ���� ���� ������5.36 :��� ���� ����� (���� ���� ���� ��� (�)NSI � ����� ����� ������� ����- (�)5.36 ���� ��� �� ����� .NSI ������� ����

� ��� ���� �����- 5.36 .��� �� ����� ���� ���� ,���� � ��� ,������� ���� ���� ���� ���� �� ������ ���� �� ��� ����� ����� ������ �� ���� ���

���� (��� ����� ���� ���� ��) ������� ������ ����242,537 ���� ���� ����NSI �������� � ��Habas Tulip � �������- 1.7% � �������� ���Habas Tulip �- NSI .

�� ,(����� ����� ������ �����) ������� ������ ���� � ������� ����� �� ��� ��� ���� � � ����� ��� ������� ����� ,����� ���� ������� ������ ������ �������5% . ���

������� ,������� ����� �����Habas Star ����� ���� �� ������ ����� �� ��Habas Star ,

���� ��� ���� ��� �� ��) ���� ������� ���� ���� ����� ������ ��� ��.(�� ���� ���� �� ��� ����� ,� ��� ������� ����� ������� ���� ������ ���� �� ���NSI

� � �� ��������Habas Tulip.� ��� ������� ���� ����� ,����� � � �� ,

�. ������� ���2012 ���� �� ��� � � ����� ������� � ���� ���� ,�"��- 64% ��) ����� � � �� :�� � ��� ���� ����� ������ ("���� ��"25,500 ���� ��� ������� �� �� ����� ������) �" ����13 �

� � �� ���� ��� � ���� ������ �������� ��� ������� �� �"� ������� ���� .(����� ���� ������ ����� � � �� � ���� ������ ������� ������ ��� ��� ���) � � ���Ltd Investments Coronell

�� �������- 21% " :����) ���� �� �����Coronell"(( ���� �� ��������� � � �� ����� ����� ����� ����28 ����2013 ,���� ������ ����� ������ ������ ������ ���� �� ����� ���� �� ���� ��

��� �� ��� ����� ��� ���� �� ������ ������� ���� ����� ���� �� �� �� ��� ���� ��� �� ���� Coronell � ���� �� ���� � ���� ���- Coronell .���� ��� ��� ,����� ����� ���� ��

� �� ,���� ,"����� �����"8.5 ������ ������� ������ �� ����� �� � ���� ����� ������ �"��� ������� ���� �� ���� �� ���� �� ��- Coronell ��� ���) ����� ������� ������� �����

���� ��� ����� ������� ���� ��� ��� ���� ���� ,���� ,"����� ������� �������" .(���� '�� ����� � ������ ��� ����1 ����) ����� ���� �����7 �������2010 �� �� �� ( ���� �� ����

��� ����7 �������2010 ��/� ���� ��� ���� ��� ����� ����� ��/� ����� ������� ������ ��/� ����� ������� �� �� ��� ������� ������� ��� ,������ ����� ���� ����� ����� �����

� �� ����� ����� �����6% �� ���� ��� �� ��� ���� ��� ���� ���� �� �� ��� �� ����� ��� �� ������ �� ����� ����� ,����� ����� ������� ������� ����� ����� .(����� ���) ����� �� ���� ����� � � �� ���� ������ �����) ����� ����� ��� ���� �� ��/� ���� �� ���� �����

� ��� ����� ����� ���� �� � ���� � � �� ���� ����� �� (����� ����� ���� ��� ���Coronell , .����� ���� ���� ������ ��� ���� ��� ����� ������ ������� �� ��� ���� �����Coronell ��

.������ ������ ��� ����� ����� ����� ���� � ����� ��� ����

� ����� ����� ���� ������ ���� ��� �� - Coronell ����� ������ ��� �� ���� �� ���� ,����� ��/� ����� � ���� ��/� � ���� ������ ������� � �������Coronell ���) ���� ��� - ��� (���

.��� ����

,��� ����� ����� ����� ����� ����� �� , ���� ����� ���� �� ��������� � � �� ����� �� ����� �� ����� ����� �� ���� ���� ���� ,����� ��-14 ���� ,����� ������ ���� ���� ����� ���

����� ,�������� ��Coronell � ��� ����� ,������� �� ���� ��� � ��� ��� �� ,8.5 ������ �"���� ���� �� ���� ����� .����� ������� �� ��� ���� �� �- Coronell ����� .�����

) ����� ���1960����� ������ (

(������ ���) ������ ����� ������� ����� ������ �����

16

���6 - ��� ����� ������� (����) .� (���)

���� ����� ��� ����� ��Coronell '�� �����" :����) ����� ���� ���� � ��� ������ ����� �� ,2 �� ("������� �� �� �� ����� ���� ���� ���� ������ ���� Coronell �� ��- �"�� ������ ����

�������) �- 15% " :����) ���� �� ������� �� (("- 10% �� ,���� �� � ����� ����� ���� ���������� ,��� Coronell �� �� ��� ����� �� �� ��� ����� ��������� � ����� ������ ���� �����